Coffee lovers tend to pledge strong loyalties to their favorite coffee shop, often stronger than loyalties to a professional sports. Sound familiar? Well, if this is you, could your allegiance to your favorite coffee shop be swayed by knowing how it treats its suppliers and contractors?

What if you knew their business credit scores, which are a reflection on how they handle their finances and debts? If so, take a look at the scores of major coffee shops Starbucks, Peet’s, Philz, and Dunkin’ Donuts to find out which has the best business credit score. (Note: Representatives for the companies did not immediately respond to requests for comment.)

What’s a Business Credit Score?

Similar to personal credit, business credit scores and reports offer one way to determine the credibility of a company by looking into how it has handled debts and obligations in the past.

As a business makes payments on business credit cards, loans, trade accounts with suppliers, etc., those payments may be reported to various warehouses that collect business data. Business credit reporting agencies use that data to create a score, which suppliers, vendors and even business partners can look up.

These scores can determine a business’s ability to qualify for funding or trade terms, large work contracts, rates on insurance premiums and more.

How did we get our hands on these coffee giants scores? Well, here’s a wild fact: Anyone can look up a business’s credit score, any time they want, without notifying or getting permission from the business. Here are the scores (and what they mean) for the four major coffee shops we mentioned. (Note: All scores are on a 0 to 100 range and are as of Nov. 17, 2016.)

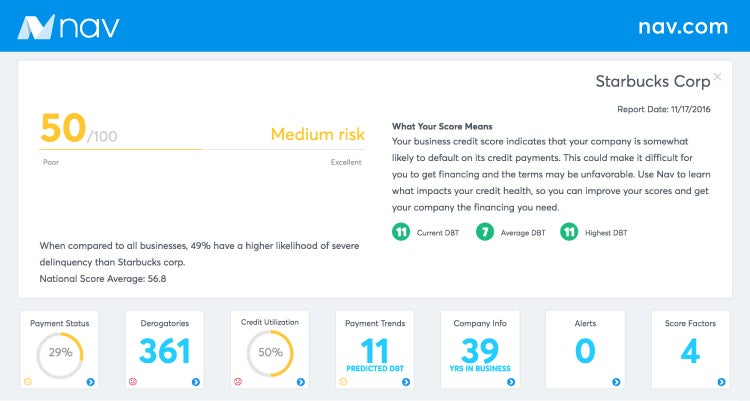

Starbucks

Starbucks Corp.’s business credit score was a 50, putting it in a medium risk category. The national score average is 56.8.

The most important factor influencing this score is payment status, which accounts for approximately 50% or more of the score. Payment status, however, works differently from that of personal credit — instead of a 30-day grace period, a payment that is even one day late can be reported on a business credit report as a slow or delinquent payment.

The report shows that of all the accounts listed for Starbucks, close to 30% of them have a delinquent status. Starbucks is also using 50% of its total available credit. Both the high number of delinquent accounts and the high debt usage can signal financial risk and reduce the score.

The report also shows that Starbucks Corp. has 361 derogatory marks, 277 of which are accounts that have been turned over to a collections agency. Derogatory marks are also likely bringing down their score. Of those collection accounts, 238 of them are listed as paid in full. More than 200 of them are from the Environmental Control Board. It’s important to know what these accounts are — they could even be duplicates or mistakes negatively affecting the score.

The other derogatory remarks include 60 state tax liens and 23 judgments, which indicate a financial obligation to pay any court-ordered damages following a lawsuit in which the business was the defendant. Both of these can hurt a business’s chances of qualifying for the best financing products and most flexible terms.

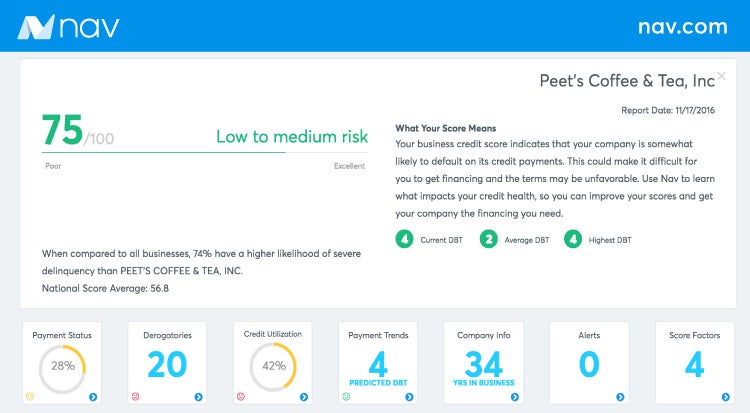

Peet’s Coffee & Tea

Peet’s Coffee & Tea’s credit score was a 75, putting it in a low- to medium-risk category, well above the national score average.

Peet’s Coffee & Tea’s credit score was a 75, putting it in a low- to medium-risk category, well above the national score average.

Of Peet’s 56 accounts reporting, 16 of them show a delinquent status. There are seven tax liens and 12 derogatory UCC filings, as well as one account that has been turned over to a collection agency and is listed as paid in full (these can stay on business credit reports for more than six years, even if paid).

This score shows that Peet’s generally pays its creditors on time or just a few days late, which is usually an indication that a business is financially healthy and considered low risk.

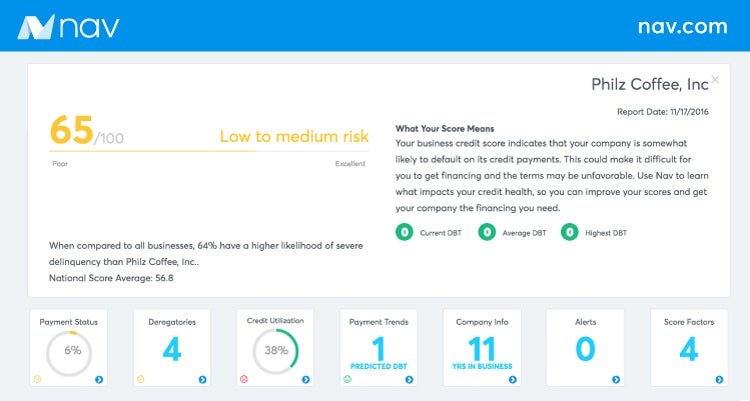

Philz Coffee

Coming in hot with a score between that of Peet’s and Starbucks is Philz Coffee, with a score of 65. This score puts Philz in the same low- to medium-risk category as Peet’s.

Coming in hot with a score between that of Peet’s and Starbucks is Philz Coffee, with a score of 65. This score puts Philz in the same low- to medium-risk category as Peet’s.

Philz has a smaller number of accounts than the above competitors, with 15 accounts reporting and only one showing a delinquent status. Other factors that might be bringing down Philz score include one state tax lien, UCC filings that are listed as derogatory and even the age of the credit file. Philz has 11 years in business, according to the business credit report, while Peet’s and Starbucks each have more than 30 years. A credit file showing fewer years in business can indicate less certainty about the future of the business.

The payment trends section of the report shows that Philz pays its bills approximately on time or only a few days late. This is a good indicator of financial health to creditors and is likely having a positive effect on the score.

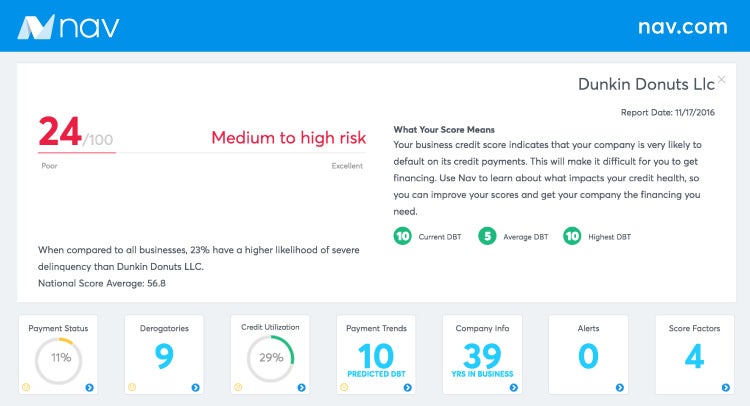

Dunkin’ Donuts

Dunkin’ Donuts’ score is a 24, which puts the business in a medium- to high-risk category.

Dunkin’ Donuts’ score is a 24, which puts the business in a medium- to high-risk category.

Dunkin’ Donuts has one account that is beyond the terms of the agreement, according to the report. The report indicates that the low number of active accounts in the past 12 months could be a factor bringing down the score, as well as the multiple tax liens, derogatory UCC filings and a judgment.

Although Dunkin’ Donuts is carrying revolving debt (29% debt usage), it is likely low enough not to have a large negative impact on the score (however, it is always best for businesses pay balances in full, if possible). Dunkin’ Donuts also has a long established credit history, which predicts continued success and has a positive impact on its credit scores.

Another Scoring Factor

One interesting factor that may influence how each of these coffee producers is viewed in the eyes of lenders is their industry classification, or SIC and NAICS codes. Dunkin’ Donuts, for example, has an SIC code associated with “doughnuts,” which is a low-risk industry, while Peet’s, which is listed under “coffee, roasted,” is a medium-risk industry.

Some small business SIC codes that are higher risk can trigger a reduced credit limit recommendations or even an automatic decline from lenders. If you’re a small business owner checking your scores, you’ll want to know how the bureaus are classifying your business and what impact it might have on your credit.

Score Higher Than Your Favorite Cup of Joe

For most businesses, establishing business credit is the first step toward building strong credit scores. Separating personal and business expenses, as well as obtaining a business credit card or accounts with vendors and suppliers that report to commercial credit agencies are great first steps. As you start to make payments on your accounts, be sure to make them on time or even early.

It’s important to check your credit scores. (You can see two of your personal credit scores for free, updated every 14 days, on Credit.com.) Be sure to look for any errors or misinformation — make sure the accounts listed are associated with your business, and make sure you don’t have any tax liens, collections accounts, judgments, bankruptcies or UCC filings that shouldn’t be there. Inspect your company information, like your SIC code, to make sure you aren’t incorrectly identified as a higher-risk business.

Next time you sit down with your favorite cup of joe, consider setting your news app aside and take a close look at your credit reports and scores instead. Knowing where you stand and taking steps to improve it will energize your business and help keep you ahead of the pack.

Image: Georgijevic

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized