The home equity line of credit (HELOC) had been around for many years before it became a hugely popular financial product in the early 2000s. When the financial crisis happened in 2008, drastically lower home valuations put a stop to the HELOC boom, and today we see far fewer being issued by lending institutions. However, millions of homeowners still have this type of contract and will face major problems when their HELOCs reach a 10-year reset point in 2015-2016.

The Office of the Comptroller of Currency (OCC) defines a HELOC as “a dwelling-secured line of credit that generally provides a draw period followed by a repayment period.” If you don’t know what these terms mean, then it’s time to have a fresh look at your contract. As a debt relief consultant who includes second mortgage and HELOC settlement negotiations in my practice, I routinely encounter clients who are worried about their homes having negative equity, but seem completely unaware of their looming reset problem.

There are numerous types of HELOC agreements, but one common variation is the 25-year contract, with a 10-year borrowing period and a 15-year repayment period. Let’s say you obtained a HELOC in 2005 that was structured this way, and borrowed $50,000 on your house to pay off other bills, do some home improvements, and so on. This whole time you’ve been paying interest-only at 6%, which is high compared to today’s rates, but since you are only paying interest on the principal balance, the payment is still manageable at only $250 per month.

What will happen at the end of your 10-year borrowing period? The line-of-credit feature of the HELOC will expire and the payments must then increase during the repayment period to cover repayment of the principal balance (plus ongoing interest). At a 6% annual percentage rate, the $250 per month payment will suddenly spike to $492 and remain at that level until the $50,000 is paid off (assuming a fixed interest rate).

This of course illustrates a 15-year repayment period, which is already greatly compressed compared to a traditional 30-year mortgage. Worse, some HELOC products were set up for a total contract duration of 15 years, meaning a 10-year borrowing period followed by only a 5-year repayment period. With such a short period of time to repay principal, the monthly payment in our example would jump to $967 after reset, almost four times the interest-only level. Talk about payment shock!

Still other types of HELOC contracts carry no repayment period at all. They were set up for a borrowing period of 5, 7 or 10 years, and at the end of that period the entire principal amount falls due in the form of a single lump-sum balloon payment. Using our same example, at the end of 10 years, instead of paying $250/month, you now owe $50,000 in a single payment.

Such financial products were built on the crucial assumption that real estate values would continue to rise, which would allow qualified borrowers to refinance to more favorable terms within a few years anyway. Essentially, these products were designed with the expectation that borrowers would extinguish the loans before reaching the point of reset, especially if there was a balloon payment rather than a reasonable repayment period.

Fast forward a few years, and the steep plunge in real estate values has left countless homeowners in a position where traditional refinancing is simply not available, thus exposing them to future payment shock when their HELOCs reset in 2015 or beyond. Since so many HELOCs were issued in 2004 through 2008 compared to prior years, the “HELOC reset” problem has the potential to affect America’s housing recovery for years to come.

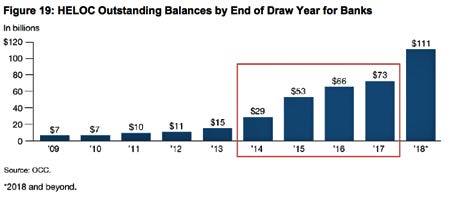

According to the OCC, in 2012 approximately $11 billion in HELOC loans reached reset point, with “reset” defined as the point where the borrowing period ended and the repayment period began. By 2014, that figure had grown to $29 billion. It will nearly double again to $53 billion in 2015 and could exceed $111 billion by 2018. Between 2014 and 2017, approximately 58% of all HELOC balances are due to start amortizing.

In the next few years millions of homeowners will face the HELOC reset problem and resulting payment shock. Many will have the ability to accept the higher payment after reset, or they will refinance to a new mortgage with more favorable terms. Others may already be planning to sell the home, either via traditional or short sale. But there will still be a large pool of homeowners who find themselves facing a true financial dilemma — a contractual trap based on a product designed years ago in a different banking era, before the “new normal” of underwater property values and strict loan-to-value ratios.

Options If Your HELOC Loan Is Due to Reset in 2015 or 2016

With all that in mind, let’s focus on potential solutions for homeowners facing HELOC reset. First, if you are not sure whether this is happening with your loan, please take a close look at your agreement document. Look for the dates pertaining to the Borrowing Period and the Repayment Period, bearing in mind your contract might use slightly different terminology. If you took a loan in 2005, for example, it’s likely the reset will happen in 2015.

Once you have confirmed the date on which your HELOC will reset, the next step is to determine the new payment schedule including principal. If you have not already received a notice from your lender with this information (many lenders are sending these out well in advance to warn consumers about the pending payment increase), then you should be able to determine the new payment from the contract terms and the help of a loan or mortgage calculator. Or, perhaps much easier, you can simply call your lender and ask them what the new payment will be after reset.

1. Absorb the New Payment

Using our first example above, some household budgets can tolerate a payment spike from $250 to $492 per month. If you can fund the new payment and otherwise don’t have any refinancing options available to you, then why not give the new payment a try for 12 months? See how you do before considering an aggressive solution that may entail serious credit damage.

2. A Traditional Refinance

Some homeowners facing HELOC reset will be able to obtain new mortgage financing that solves the problem. By combining the original first mortgage and the HELOC balance into a new single mortgage, all risk associated with the HELOC reset is extinguished with closing on the new note.

Of course, many homeowners will be blocked from this solution, based on three key factors:

- Lenders require a loan-to-value ratio of 75-80%, so the property has to be worth enough at market value to offset the two combined notes and still leave 20-25% equity as a cushion. Many homes are still upside-down in value, worth less than the two note balances combined, or perhaps worth less than the first mortgage alone.

- Your credit score has to be in excellent shape to qualify for the best rates. (You can see two of your credit scores for free on Credit.com.)

- Your income has to support the new revised mortgage payment, based on strict debt-to-income ratio formulas.

Unless all three conditions are in place, a traditional refinance solution won’t be available to you.

3. Modify Your First Mortgage Under HAMP, or Second/HELOC Under 2MP

Although it was announced with some press attention a few years ago, it’s rare to see the government’s Second Lien Modification Program (2MP) discussed in the context of the HELOC reset problem. Government sponsored programs like the Home Affordable Mortgage Program or Home Affordable Refinance Program (HAMP and HARP) targeted mainly first mortgages, in an effort to stabilize payments so people could stay in their homes or refinance away from toxic mortgages.

While HAMP and HARP have helped millions of homeowners over the past half-decade, the 2MP has been something of a mystery. It’s common to hear someone report having successfully modified a first mortgage via the HAMP solution. Yet reports of successful second lien modifications under 2MP are quite rare. If HAMP modifications have proceeded like a gushing pipeline, 2MP modifications are more like a tiny trickle.

According to the Department of Housing & Urban Development (HUD) website, you may be eligible for 2MP if your first mortgage was modified under HAMP and you have not missed three consecutive monthly payments on your HAMP modification. What this should mean, at least in theory, is that once you have finished making your three trial payments under an approved HAMP modification, then your second lien should be reviewed for a corresponding modification.

Check with your lender directly to see if they are participating in the Second Lien Modification Program. I would also encourage readers looking for more information on the government-sponsored programs like HAMP, HARP and 2MP to call a HUD agency counselor at 1-888-995-HOPE (4673). There is no cost to you, and the HUD counselor can help determine eligibility for one of these programs.

4. Modify Your First Mortgage, Then Apply the Savings to the Payment Spike

A successful loan modification on your first mortgage can result in significant monthly savings. If you modified under HAMP but your second lien did not qualify for 2MP, or you did a non-HAMP modification directly with your mortgage lender (also called an in-house or a private modification), then your first mortgage payment should now be lower than it was previously.

In some cases, the difference may be sufficient to offset some or most of the expected payment spike associated with a pending HELOC reset. Your budget will naturally determine this. If you pursued the modification due to financial hardship, then it may be that even with a lower first mortgage payment you still can’t handle the increased HELOC payment after reset. But others will find that the savings achieved through the first mortgage modification provides enough relief that the payment increase on the HELOC will no longer cause such a severe budget problem.

5. A Loan Modification Directly With the HELOC Lender

There are many situations where none of the above solutions will apply. What if you can’t absorb the new payment after reset or you have a balloon payment coming up? What if traditional refinancing is not available to you because the house doesn’t meet the required loan-to-value ratio? What if none of the government programs apply? What if modifying your first mortgage won’t or can’t work, now what?

Lenders do not want a default to occur. A logical step would be to determine precisely what in-house programs your creditor is willing to offer and see if any of these options look realistic to you. Financial institutions have been issued a strongly worded guidance by the OCC on the subject of HELOC reset, and they want servicers to work with customers to salvage these loans. So it makes sense to find out what the servicer is offering for modified terms and then compare to the original payment spike.

To get anywhere with a loan modification application, be prepared to submit two years of tax returns, bank statements, pay stubs and a personal financial statement. Be patient and polite. Do your own math before you approach the servicer for a modification. Know what you want in terms of a payment and loan duration, including possible principal deferment or even principal reduction, before you enter the negotiation. You may or may not get exactly what you want, but it pays to know your own figures and to be able to argue your case effectively.

6. Strip the Lien via Chapter 13 Bankruptcy

Bankruptcy is an aggressive solution that would only apply in specific circumstances. I mention Chapter 13 bankruptcy specifically because it has a unique feature that allows a second lien to be stripped from a property. This can only happen if the property appraises for less than the balance owed on the first mortgage, and of course with the court’s approval. If the lien strip is approved, the HELOC or second mortgage balance then becomes an unsecured debt co-equal with other unsecured debts like credit cards, medical bills and so on. The debt is then discharged after the case is completed, with five years being the typical Chapter 13 case duration. The advantage of this solution is that it yields a one-mortgage property with no further threat of foreclosure or potential litigation. It’s crucial to get the advice of a good bankruptcy attorney if your intention is a lien strip via Chapter 13.

7. Lump-Sum Settlement

Settlement is also an aggressive strategy that comes with credit damage and only applies in specific circumstances. There are tax consequences of settlement, in the form of a 1099-C for the forgiven balance, taxable income unless an exemption applies.

During the peak years of the real estate crisis many homes plummeted in value to a level below the balance owed on the first mortgage alone. That left second lien holders in a position without collateral, i.e., “underwater.” Under such conditions, many homeowners were able to settle their HELOCs for 10-20% of the balance after having defaulted for an extended period.

While HELOC settlements are still happening in 2015, conditions have changed considerably. We are now in an era of rising property values, and creditors are more reluctant to absorb a loss when the property underwater today may be “in the money” again before too long.

As a debt consultant, I find I’m recommending the settlement strategy for HELOCs much more selectively than I did in prior years. It does still work quite effectively in many situations, but it’s important to have a clear view of the risks before attempting a hardball negotiation strategy like debt settlement on a second mortgage or HELOC.

The bottom line is there is no single best debt relief solution for the problem of HELOC reset. I’ve presented seven potential strategies above, but each of those will only apply under specific financial conditions. Aside from the sister program to HAMP, the 2MP for second liens, there are no “Obama programs” for HELOC relief, and no bank sponsored programs to enroll in. Based on hundreds of consultations with consumers struggling with HELOC issues, my experience has been that creditors are taking a battlefield management approach, with the goal of stemming further losses. So beware of companies or services claiming they can have your lien extinguished, or have your HELOC note declared invalid. The growing HELOC reset problem presents a new opportunity for debt relief scammers to pitch bogus programs that promise to “make your HELOC go away.” Buyer beware!

More on Mortgages & Homebuying:

- Why You Should Check Your Credit Before Buying a Home

- How to Find & Choose a Mortgage Lender

- How to Refinance Your Home Loan With Bad Credit

Image: iStock

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages