Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

300 is the lowest credit score that a person can have. It’s impossible for a score to drop below 300 for any reason.

Learning how credit scores work can be mystifying, especially if you’re establishing credit for the first time. 42% of Gen Z don’t fully understand how credit scores work, which can lead them to ask questions like “What is the lowest credit score?” 300 is the lowest credit score anyone can have—but there’s a difference between knowing your score and having a plan to improve it.

We’ll discuss credit scores and credit ranges in this guide, and we’ll share five steps for improving low credit. Building credit can pave the way for tons of great opportunities like low-interest loans and premier credit cards.

What Are the FICO Credit Score Ranges?

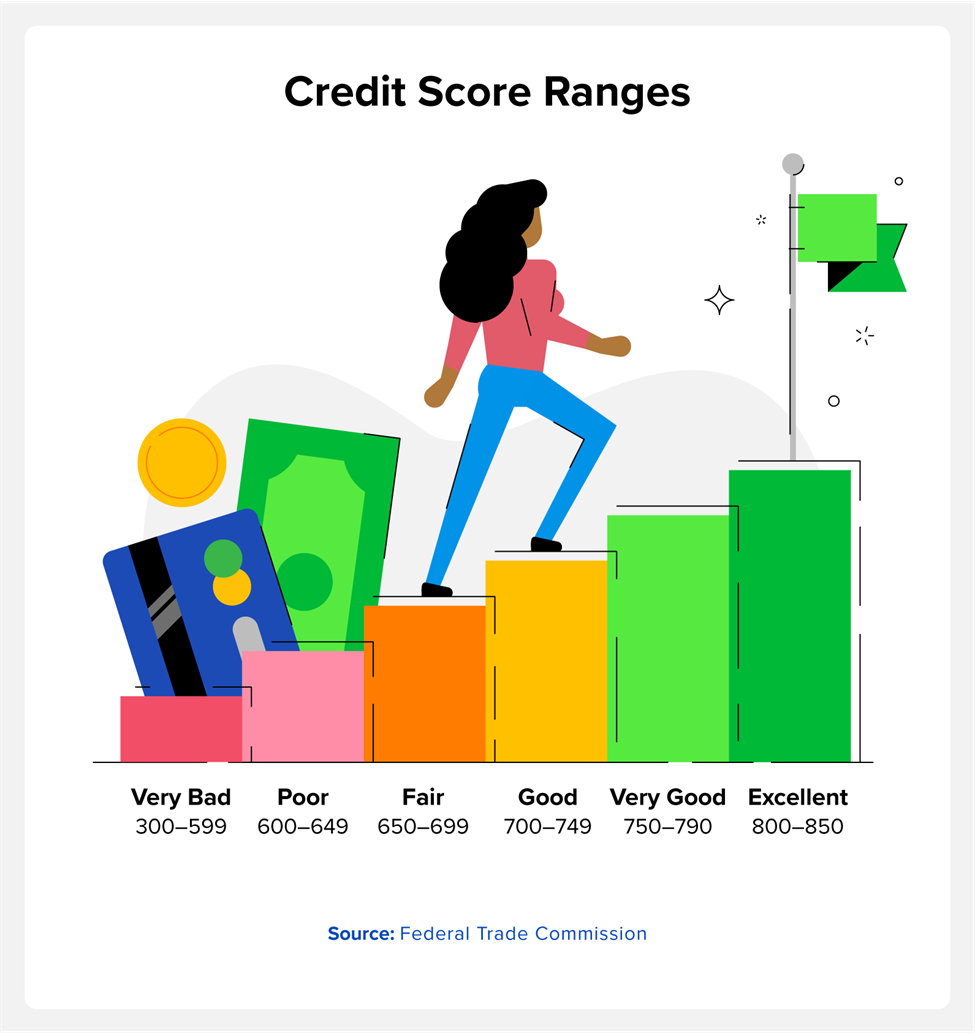

Credit scores typically fall into five different ranges—Poor, Fair, Good, Very Good, and Excellent. Each range encompasses a set value of credit scores; the “Poor” category covers the widest range of credit scores and while the “Excellent” section covers the smallest range.

Different credit agencies and websites generally classify credit score ranges similarly, with slight variations. More often than not, you’ll encounter the following information:

- Poor (300-579): 300 is the lowest credit score a person can have, and it’s impossible to drop below that number.

- Fair (580-669): Lenders and banks will look at a Fair score more favorably, but their best offers may still be out of reach.

- Good (670-739): Experian® reported 714 as the average credit score in 2022.

- Very Good (740-799): Keeping your credit utilization ratio low and consistently making payments on time can contribute to a Very Good score.

- Excellent (800-850): Approximately 1.3% of Americans have Excellent credit. Excellent credit isn’t necessary to attain great loans per se, but it’s a worthy goal to strive for.

The Risks of Having a Low Credit Score

Lenders, real estate agents, banks, and loan agencies use our credit scores to gauge our financial trustworthiness. These entities may interpret “Poor” and “Fair “scores as a sign that someone either won’t make their payments on time or at all. Securing a loan can be very difficult with Poor or Fair credit—and even if you do, that loan will have significantly higher interest rates.

A low credit score also makes it difficult to increase your credit limit in several ways; most banks are hesitant to offer new cards or grant a credit limit increase to Poor or Fair credit applicants. Lastly, many landlords will turn down applicants with credit scores below a certain threshold.

How to Get a Loan with a Low Score

Securing a loan with a low credit score can be challenging, but it’s not impossible. Nonprofit organizations like credit unions can accommodate clients with Poor or Fair credit. It may even possible to acquire a mortgage with bad credit if your score is hovering above 580.

Be wary of scams and fraud when searching for low-credit loans; cybercriminals may try to glean sensitive information by imitating legitimate lenders. Prudence is your best bet—research the person or organization that you’re speaking to by looking them up online to verify their identity before providing your SSN.

Actions that Could Improve Your Credit Score

There’s only one direction to go if you’re at the bottom, and that’s up. Someone with a score of 300 can repair their credit by making plans and taking action. The following five steps can help you start on the road to recovery from even the lowest credit scores—and stay the course as things improve.

1. Get Your Free Credit Report

Equifax®, Experian, and TransUnion® are America’s most significant credit bureaus. These agencies provide reports about our credit history, and the law requires them to provide one free credit report each year.

Credit.com also provides free credit scores, plus a credit report card that grades your credit activity and offers practical feedback.

2. Challenge Errors on Your Report

Everyone makes mistakes, including credit lenders and credit bureaus. If you find false or inaccurate information on your credit report, you can challenge the accuracy of these blemishes. Contact the corresponding credit agency and company that made the mistake and respectfully request assistance.

3. Avoid Hard Inquiries

Hard credit inquiries result from lenders and agencies looking at your credit history when you apply for a card or a loan. Inquiries don’t stick around forever, but they can significantly inconvenience you by making your score seem lower than it really is.

Don’t apply for too many new cards while working to improve your credit. A mistimed hard inquiry can make the difference between securing a loan and having to wait months to try again.

4. Pay Down Your Debt from Largest to Smallest

Paying off your debt will always be one of the best ways to improve your credit—it’s more a matter of figuring out how to best go about doing so. As tempting as it may be to pay off your smallest accounts, paying off your largest debts will make the largest difference on your credit report.

Large debts contribute to your credit utilization ratio the most, so paying them off will free up tons of space. A large debt might also belong to one of your oldest accounts, and time is a significant factor that impacts credit. Whittling down a massive loan over time could tangibly boost your score in real time.

5. Utilize Credit Repair Services

Credit repair services excel at helping people create practical plans to work to build their credit. ExtraCredit® offers several features to help you manage your credit, including an exclusive discount to a leader in credit repair.

Low Credit Score FAQ

Is It Possible to Have a Credit Score of 250?

It is impossible for a person’s credit score to drop to 250, as 300 is the lowest number that the major credit bureaus standard modeling will recognize. However, a person’s specialized FICO® score, specifically their Auto Score and Bankcard score, can range from 250-900 as they focus on more specific areas of your credit. Auto and Bankcard scores help lenders decide if they’ll offer you an auto loan or credit card, respectively.

What Happens If I Have a Credit Score of 300?

A credit score of 300 will make it difficult to secure auto loans, home loans, and credit cards from respected lenders. Poor credit scores also can affect insurance premiums and interest rates.

Can I Buy a House with a Low Credit Score?

It’s certainly possible to gain a home loan with a low credit score—but the process may be much more difficult. Federal Housing Administration (FHA) loans can be monumentally beneficial to individuals with Poor or Fair scores. However, you may need to make a larger down payment.

Stay on Top of Your Credit

The most important step you can take to improve your credit score is to stay on top of your credit report. You can request a free credit report from all three main credit reporting agencies—Experian, Equifax, and TransUnion—once a year.

The details on these reports can help you make sure everything on your credit report is accurate and up to date. Make sure you take the appropriate steps to remove any inaccurate information from your credit report. Additionally, having access to your report and credit score can help you determine what areas you need to focus on to rebuild your credit.

To get your free Experian Vantage 3.0 credit score, you can also sign up for Credit.com’s free Credit Report Card.

You Might Also Like

Experian is a credit reporting agency. It also offers consumer cr... Read More

March 7, 2023

Credit Score

Do you keep a close eye on your personal finances? Or maybe you�... Read More

January 4, 2021

Credit Score

If you’re serious about your credit score, you need to pay your... Read More

September 29, 2020

Credit Score