More and more apartment buildings are popping up in cities around the country, but that doesn’t mean they’re getting more affordable. A large number of these developments are very upscale, aimed at people who can afford some serious luxury.

That’s the finding of a recent study conducted by RENTCafé, a nationwide apartment search website.

The study found that 3-in-4 new apartment developments built in 2015 were high-end rentals, and that luxury construction was up 63% overall from 2012. In absolute numbers, that translates to 896 luxury multi-family projects of 50+ units (out of a total of 1,188 total projects) completed in 2015, according to RENTCafé, compared to 382 luxury multi-family projects of 50+ units completed three years prior.

Early 2016 data shows no slowdown in luxury apartment development, with 79% of all apartment buildings finalized in the first quarter of 2016 being categorized as luxury.

Renting: The New American Dream?

A 2015 report by the Urban Institute projected that even after the housing crash and the Great Recession are a distant memory, homeownership rates in America will continue to decline.

The report estimated that between 2010 and 2030, the majority (59%) of the 22 million new households that will form will rent, while just 41% will buy their homes.

The homeownership rate has been falling since 2006, when the housing bubble began pricing out many would-be homeowners — and the recession furthered that trend. In 2006, the homeownership rate was 67.3%; it now sits at 63.6%, even lower than it was in 1990, according the U.S. Census’ most recent American Community Survey.

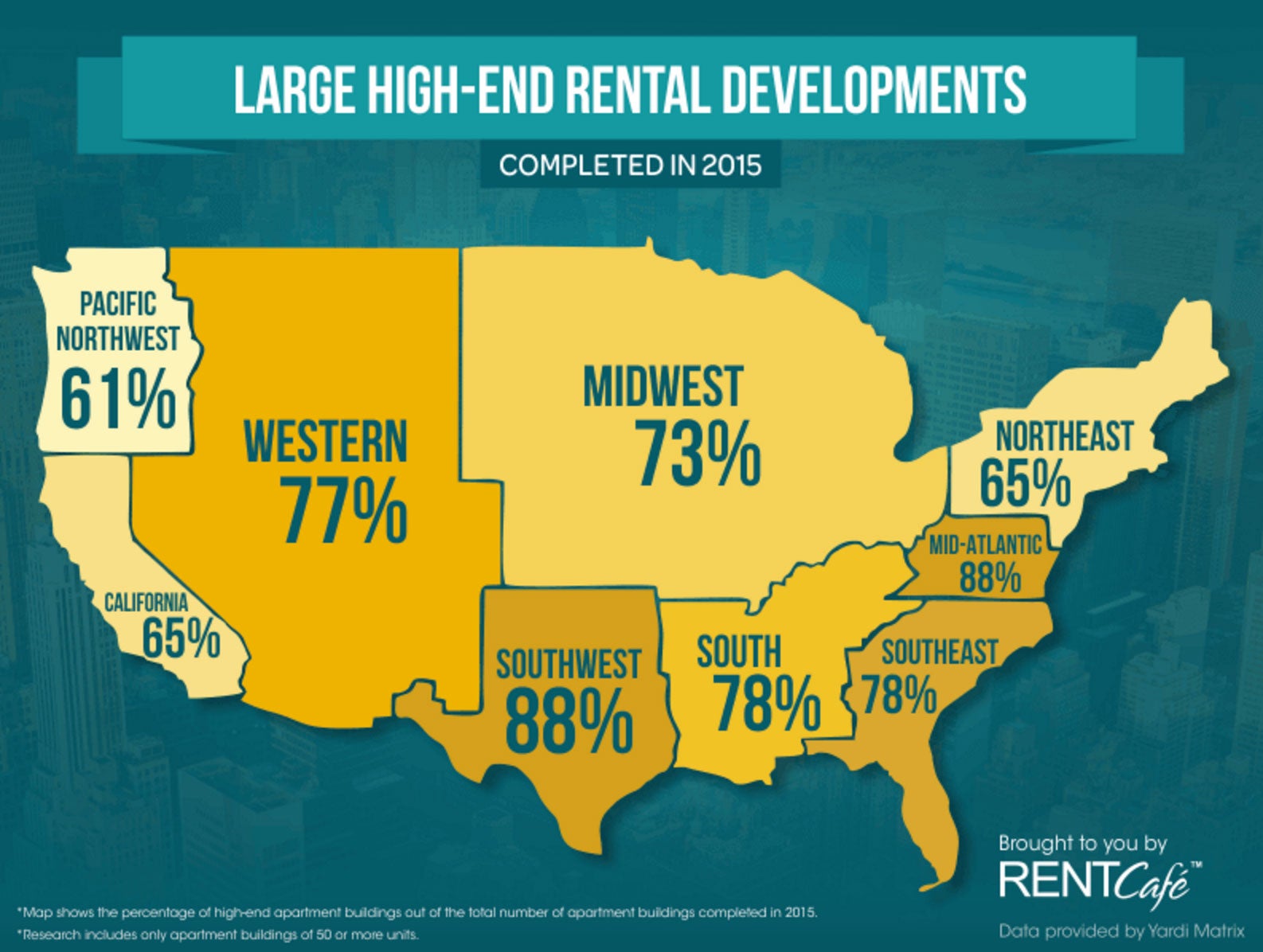

Where Luxury Grows Fastest

Given those statistics, it’s no wonder developers are focusing on rentals with amenities that typically far surpass those available in starter homes. The highest percentages of high-end rentals were registered in the Southwest and the Mid-Atlantic (88% of the total number of large rental developments), and in the South and Southeast (78%), the study showed. The lowest numbers were registered in the Pacific Northwest (61%), in California (65%) and in the Northeast (65%), where the leading metro markets are more mature.

Luxury apartment construction is on the uptick in all regions in recent years, however. The most significant increase from 2012 to 2015 in the ratio of high-end to total new apartments was in the Southeast, up by 119%. Over the same period of time, in the Pacific Northwest the numbers went up 90%, and in California 82%, the study showed. The lowest increase in luxury construction was registered in the Northeast – only 23% up from 2012, and in the Mid-Atlantic – 26% up from 2012.

Even with the spike in luxury apartment development, there are still cities where renting is becoming more affordable. Check out our roundup of 9 cities where rent is getting cheaper this year. Six metro areas that aren’t on that list, however, really stood out when it comes to luxury developments:

- San Antonio, Texas, where 17 out of 17 properties that completed construction in 2015 were luxury.

- Kansas City, Missouri, where 14 out of 14 properties completed were luxury, with an average monthly rent of $1,055, versus the metro average of $850.

- Milwaukee, Wisconsin, where 10 out of 10 large properties opened in 2015 were all classified as high-end with the average rental rate of $1,367 per month.

- Midland-Odessa, Texas, where 9 high-end properties were completed, charging an average monthly rent of $1,501, which is $402 more than the overall average rent.

- Jacksonville, Florida, with 7 of 7 properties completed were high-end, with average rents of $1,055.

- Oklahoma City, Oklahoma, also with 7 out of 7 properties completed in 2015 being high-end rentals with average rents of $1,090.

Finding a home or apartment to rent can sometimes be complicated, especially if you have no credit or a bad credit history. Before you start searching for a new place, get an idea of where you stand — you can get a free credit report summary every 30 days on Credit.com — and consider trying to improve your credit before you look for a new home. If that’s not an option, you may be able to find a broker or apartment-finding agency that can help you find landlords willing to work with bad-credit applicants.

More Money-Saving Reads:

Image: GCShutter

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized