It’s hard to overstate the value of emergency funds. They’re what savers tap into when life gives them lemons, and having one can often mean the difference between reaching financial goals and racking up debt.

Now a new study from the Urban Institute, a Washington, D.C.-based think tank focused on economic and social policy, suggests emergency funds are more than just a powerful cash cushion and may serve as a key indicator of cities and communities’ economic health.

As the study explains, cities and communities are only as stable as their residents’ finances. Secure families are better able to weather setbacks such as the loss of a job and are less likely to turn to local services for government subsidies. They’re also a boon to the local economy, bolstering property, sales and income taxes, and their kids are more likely to succeed, thanks to stable housing conditions, the Urban Institute said.

Low Savings Are Better Than None

In studying how savings help families survive inevitable setbacks and contribute consistently to the local economy, the Urban Institute turned up some eye-popping stats, particularly in terms of the link between family financial health and city outcomes, such as eviction, reliance on public benefits and ability to pay utility bills. These findings include:

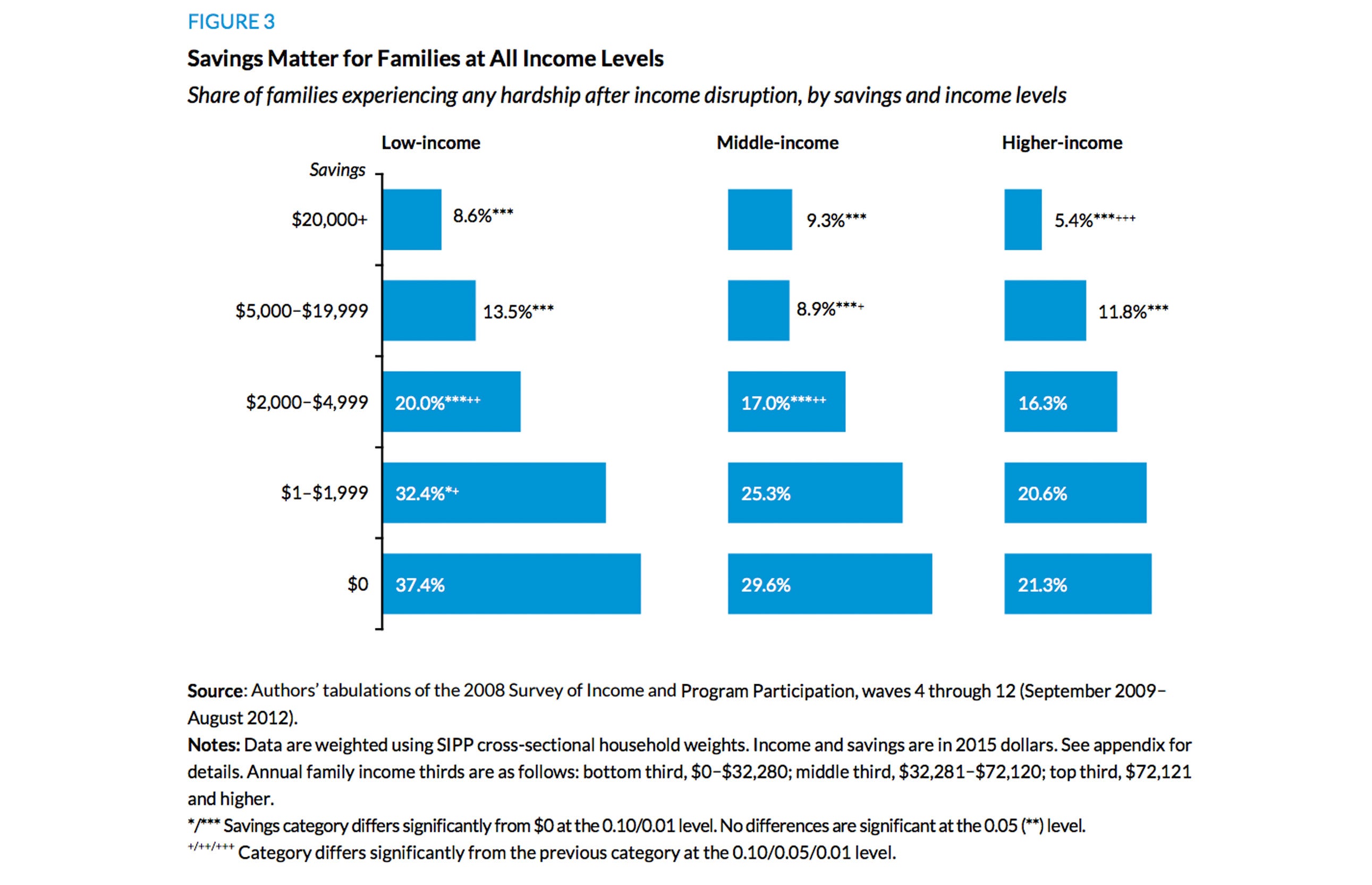

- Low-income families with savings are more financially resilient than middle-class families without savings. Low-income families with $2,000 to $4,999 stashed away are less likely to experience hardship after an income disruption than middle-income families with no savings.

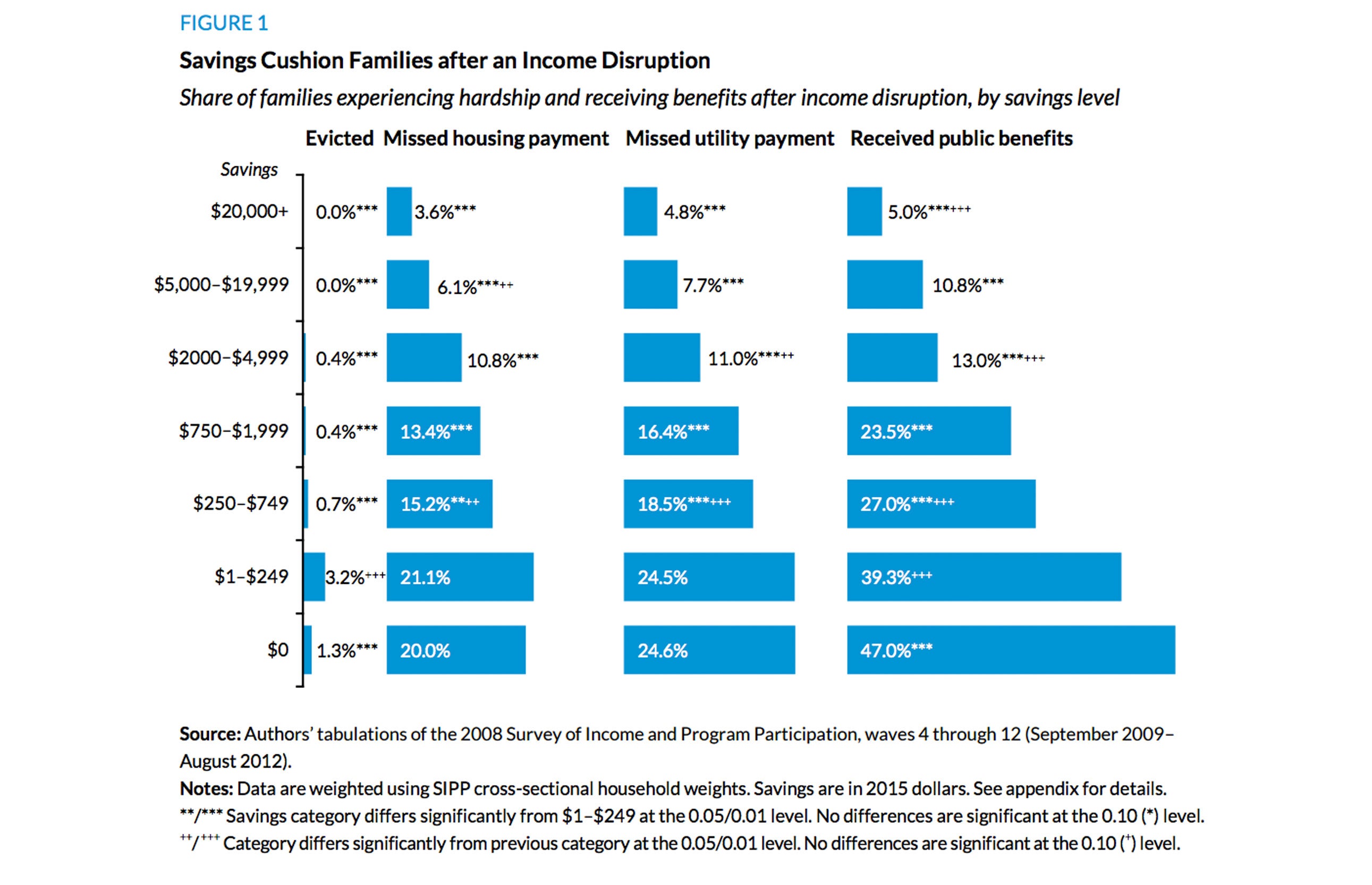

- Even low savings help. Socking away $250 to $749 has helped families avoid being evicted, missing a housing or utility payment or applying for public benefits when an income disruption occurred.

That said, higher savings are associated with lower levels of hardship, and the more a family has tucked away, the less likely it is to miss a utility payment, be evicted or turn to government assistance.

Why Families’ Financial Health Matters to Cities

About 25% of families suffer some kind of income setback over the course of 12 months, the Urban Institute found. And “almost 1 in 4 families have no nonretirement savings, roughly 4 in 10 have less than $750 and about 6 in 10 have less than $5,000,” the study said — frightening numbers given how much families’ financial health matters to cities.

Consider the impact a family’s lack of savings can have on its city over time. According to the Urban Institute:

- Evictions can lead to homelessness, which puts pressure on city budgets.

- Homelessness among children can disrupt their education, hampering their ability to succeed.

- City revenues suffer when residents have trouble paying for utilities such as water and gas.

- Crime-related correctional spending and local public welfare spending stem from family financial insecurity.

Remember, savings matter for families at all income levels. It takes at least $5,000 to protect higher-income families from income disruptions, the report found, perhaps because their standard of living is higher and they have higher fixed costs for things such as their mortgage and car payments. Low-income families, meanwhile, are more financially resilient than middle-income families without savings, the report said.

As we’ve written before, missing major payments, like a mortgage, can hinder your credit score, making it harder to secure financing for a loan, a car, future housing and much more. You can see how late payments can affect your credit score here. You can also see how any missed payments may be affecting your credit by viewing your two free credit scores, updated every 14 days, on Credit.com.

More Money-Saving Reads:

Image: iStock; Inset Charts Courtesy of The Urban Institute

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized