The Federal Communications Commission is taking a cue from the Food and Drug Administration, recommending broadband providers offer the technological equivalent of nutrition labels so consumers can have a better understanding of what goes into their service plans.

The FCC said the new labels are aimed at helping consumers compare internet and mobile service providers’ prices, performance and network practices, which “can be challenging, even for savvy consumers.”

The FCC said the new rules do not require providers to use the new label format, but those that do will satisfy the requirement to make properly-formatted transparency disclosures. Providers may still be in violation of FCC rules if their labels are misleading or inaccurate or if they make misleading or inaccurate statements to customers in ads or elsewhere, the agency said.

The new rules will go into effect later this year, but service providers may begin using the broadband label templates anytime, the FCC said. Per a news release, the data the agency wants to see disclosed includes:

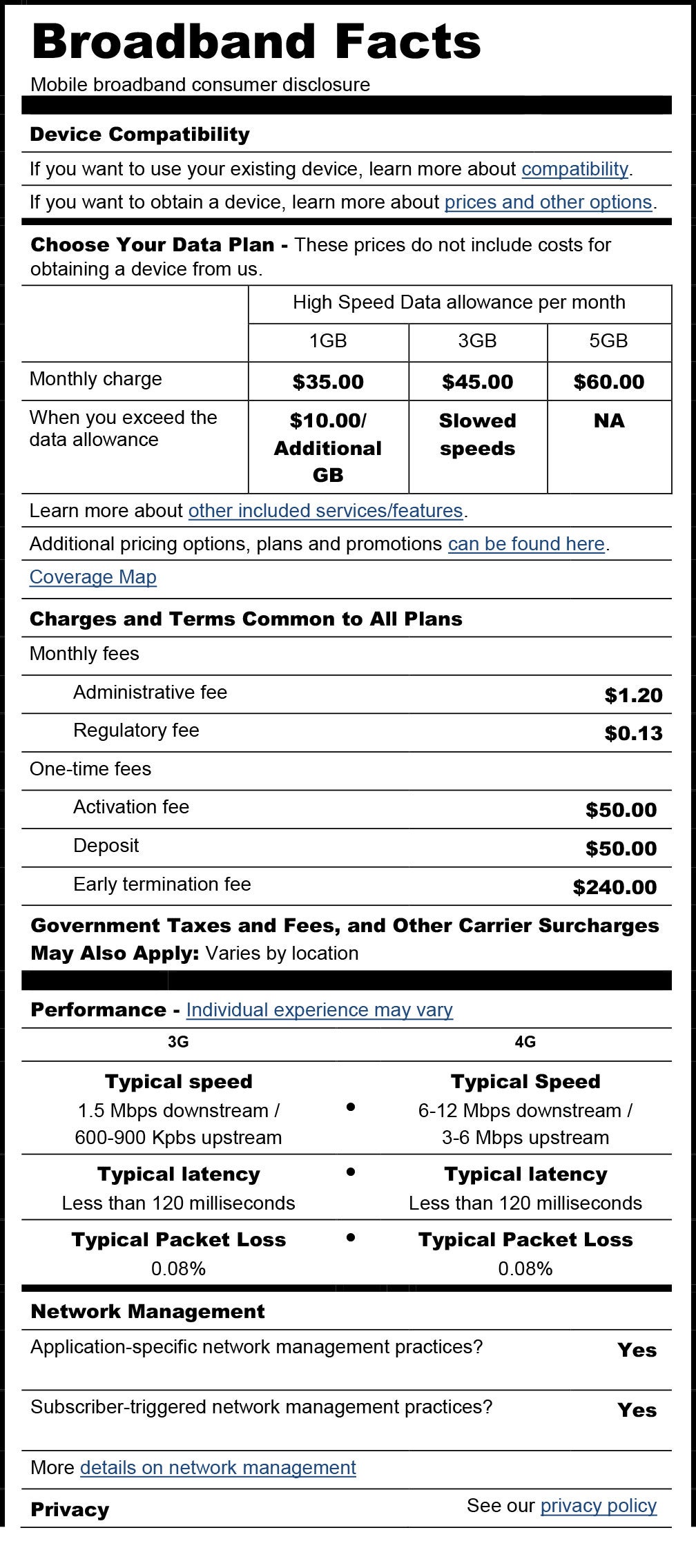

- Pricing details, including all of the various charges that seem mysterious to consumers – overage fees, equipment fees, early termination fees, other monthly fees beyond service fees such as insurance, administrative fees, or regulatory recovery fees.

- Monthly data allowance – namely, the carrier-defined plan limit after which consumers will incur additional charges.

- Broadband speed and other performance metrics.

- Network management practices – namely, precautions providers may take to manage heavy traffic on their networks.

You can see a sample of the proposed mobile broadband disclosure label below.

You can see a sample of the proposed mobile broadband disclosure label below.

Paying for Internet/Mobile Service

No matter what type of disclosure is provided, it’s important to read the terms and conditions of any contract carefully in order to determine whether you’re getting a good deal. Consumers looking to save money on their internet and mobile data plans can potentially negotiate with their current service provider, comparison-shop and consider switching service providers or downgrade to a different plan.

It could also help to improve your credit, since many Internet and mobile data providers will check a version of your credit report and often offer better rates to consumers with good credit scores. You can see where you stand by viewing your credit scores for free each month on Credit.com.

More Reads From Credit.com:

- Identity Theft: What You Need to Know

- How Do I Dispute an Error on My Credit Report?

- 3 Dumb Things You Can Do With Email

Main Image: moodboard; Inset Image: Federal Communications Commission

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized