If rising mortgage rates have spooked you into refinancing but your loan size is more than $417,000, pay particularly close attention. Traditionally, these loans cost homeowners more, but there are new investors in the marketplace offering better rates and deals on larger mortgages.

The Big Question to Ask

It doesn’t matter where you apply to refinance a mortgage — whether it’s a bank, credit union, mortgage broker or even a direct lender — the investor determines whether your loan will cost more or not.

Fannie Mae and Freddie Mac purchase loans up to the maximum conforming loan limit, designated by county – it’s often $417,000, but can be as high as $625,000 in high-cost markets. For example, in Sonoma County, Calif., it’s $520,950.

In terms of pricing, Fannie Mae and Freddie Mac loans are ideal if your loan is $417,000 or lower. However, any loan of $417,001 or more that goes to Fannie Mae or Freddie Mac will likely cost more than if it were going through a different investor. So make sure to ask your lender: “Where’s my loan going?”

Up until recently, Fannie and Freddie have been the main players for loans above the maximum loan limit. Just this year additional jumbo investors have entered the market — including Wells Fargo, Chase and many others, and they’re buying loans made by banks, credit unions, brokers and direct lenders.

Jumbo Investors Offering an Alternative

Ask your mortgage company about its “jumbo” mortgage offering. This would be especially beneficial if you’re trying to refinance a loan size bigger than $417,000 because jumbo investors specifically cater to this market.

This means that jumbos may even be lower-priced than loans $417,000 or under — which are the ones that are normally considered the best-priced mortgages in the marketplace. Working with a jumbo investor may help you avoid being subject to the pricing adjustments (a big driver of cost on mortgages) that Fannie and Freddie impose, which could help you refinance for a lower interest rate and payment.

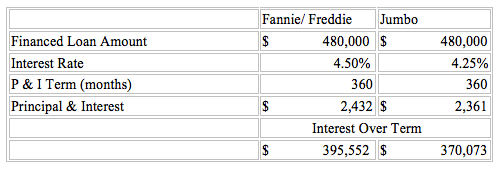

Let’s compare Fannie/Freddie to a Jumbo Investor:

Other Times the Jumbo Option May Make Sense

There are some other potential advantages to working with a jumbo investor. Let’s say you have a first mortgage on your home at $400,000 and an $80,000 home equity line of credit that you would like to consolidate into one. Fannie Mae and Freddie Mac would consider this scenario to be a “cash out refinance” because the added HELOC debt wasn’t used to acquire the home, and your mortgage company will charge you more for the loan being over $417,000 and for “cash out.” You could expect as high as .5% of the loan amount being absorbed either in the interest rate or paid for by you (based on whatever interest rate you choose) at close of escrow or paying in cold hard cash at closing.

A jumbo investor, however, will likely consider the loan in this scenario to be “rate and term,” which offers better pricing.

It’s important to remember that some jumbo investors recognize a jumbo mortgage loan to be anything bigger than $417,000. Other jumbo investors characterize a jumbo mortgage to be anything bigger than the maximum county conforming loan limit. So be sure to talk to your mortgage company when discussing jumbo loans.

Jumbo Credit Still Tight

While pursuing a jumbo mortgage refinance, credit requirements for these loan types are still relatively tight. These programs want strong borrowers with good credit, a low debt-to-income ratio and equity in the home. For example, if you’re trying to roll HELOC debt into the refinance, there can be no draws on the home equity line of credit in the past 12 months. (Before you begin your refinancing process, it helps to have an idea of your credit standing — you can get a free credit report summary on Credit.com to see where you stand.)

If you’re completing a refinance on a home that you owned for less than 12 months, some jumbo financing investors may also require you to refinance using a different loan, such as a loan issued by Fannie Mae or Freddie Mac. Furthermore, some jumbo investors have a requirement that specifically states if you’re refinancing a home that you’ve owned for less than 12 months, the original purchase price needs to be used as consideration for the value no matter what the current market supports.

Still if you plan to refinance this year, you would be well served to ask your mortgage company to qualify you on their jumbo programs, if they offer any, as well as the traditional Fannie Mae/Freddie Mac loan so you can determine which mortgage loan program will align with your payment, cash flow and equity objectives.

More on Mortgages & Homebuying:

- Why You Should Check Your Credit Before Buying a Home

- How to Refinance Your Home Loan With Bad Credit

- How to Get a Loan Fully Approved

Image: iStock

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages