CHICAGO — As I write this story, I’m stuffing my face with delicious, inexpensive popcorn I purchased from a dollar store. I don’t usually shop at such stores (in fact, I can’t remember the last time I was in one prior to my trip last week), but as a generally frugal person, I found myself curious about the sort of deals I might find there.

During the recession, sales soared at the three major dollar stores (Dollar General, Dollar Tree and the Family Dollar — the latter two companies announced a merger early in 2015). Even as the country moved out of recession, these discount retailers continued to grow, opening new stores, expanding product lines and maintaining sales increases that show dollar store shoppers aren’t going anywhere. Part of the sustained appeal is the increasing availability of name-brand merchandise, as opposed to the generic products usually associated with discount retailers.

The Experiment

I wanted to see if it made more financial sense to run errands at a dollar store or go to a big-box store (like Walmart or Target). I went to a neighborhood where, if I lived there, I could easily walk to either a dollar store or big-box retailer, so it was really a choice of which place would serve my budgetary needs best. I went to both stores on the same day — first to the dollar store — to see if I saved money by choosing the dollar store or if I would have fared better by shopping at the larger chain. It was a decision anyone living in that neighborhood might make on a weekly basis.

I went into the dollar store with an idea of a few things I wanted, but I didn’t end up sticking to my list for a couple of reasons. For example, I needed a lightbulb for an overhead fixture in my apartment, but the dollar store didn’t have the bulb I needed in stock. I like to keep scented candles in my home, and even though there were some inexpensive ones available, I didn’t like any of the scents, so I couldn’t compare those, either. I ended up buying an assortment of small things I often or regularly get when running errands. Here’s the list I used:

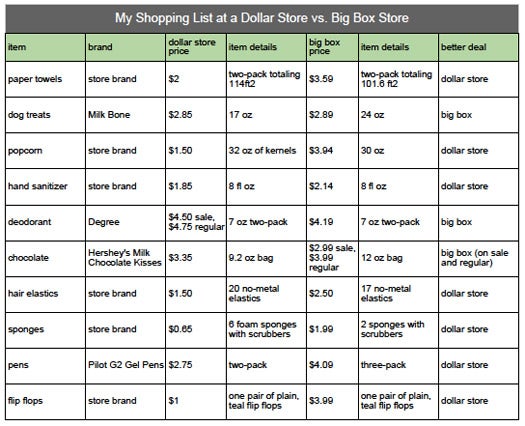

- Paper towels

- Dog treats

- Popcorn

- Hand sanitizer

- Deodorant

- Chocolate

- Hair elastics

- Sponges

- Pens

- Flip-flops

I didn’t do any price comparison with ads or on my phone; I went on my instinct of what I thought was a good deal, and in the moment, I really thought everything I bought was cheaper than what I’d find at the other store. If I bought a generic brand at the dollar store, I compared it to the big-box generic version. I compared name brands to the same brand at the other store.

What I Found

Yes, dollar stores have a lot of low-cost stuff, and I was surprised how many name-brand items were available. That being said, price comparison wasn’t the easiest thing, because nearly every name-brand item I bought was sold at a different size at the dollar store than it was at the big-box retailer. Oftentimes, a price that seemed like a good deal actually wasn’t, once you calculate the price-per-unit or price-per-ounce.

I didn’t buy several things (because I didn’t need them) that would have been good deals, like plastic cutlery, dish soap and picture frames. If I’m ever throwing a party and I want disposable dishes or serving trays, I got the sense that the dollar store would be the place to go.

Keep in mind that this was a random sample of goods, but my general conclusion from this experiment is that generics can be a great bargain at dollar stores, if you’re cool with the quality you get in return. I didn’t see any good deals on name brands, but I didn’t compare prices on every name-brand offering in the store. My advice is to go in knowing what things cost elsewhere. Here’s how the price comparison of my shopping bill breaks down:

A few notes:

Sponges

The sponges I got at the dollar store weren’t the same size as the ones at the big box store, but that didn’t really make a difference. I don’t have a dishwasher, and I used one of the dollar store sponges to do dishes for a week, and it was fine. The scrubby part started to detach from the spongy part faster than with other sponges I’ve used, but it wasn’t falling apart to the point of throwing it out or leaving debris in my sink.

Hair Elastics

They were cheaper but weren’t as stretchy as the ones I normally get. The first one I pulled out of the pack broke immediately. Still, I used the dollar store hair ties to hold my (long, thick) hair back during multiple runs, swims and bike rides throughout the week. They felt lower quality to the touch, but I couldn’t tell the difference when they were in my hair.

Flip-Flops

I wore these around my apartment building and neighborhood when taking out the trash, walking the dog or doing laundry. They’re flimsy, but comfy. As far as cheap, throwaway flip-flops go, these are definitely worth a dollar.

Popcorn

I make my popcorn on the stove and season it myself, and I didn’t notice any more or fewer unpopped kernels than I normally get with other store-brand kernels. All of the food I bought was well within whatever “best by” date the package showed.

Paper Towels

I’ve always thought generic paper towels are not as strong or as absorbent as brand-name paper towels, and these were no different. If you’re going to buy generic anyway, these were good enough and worth the savings.

Hand Sanitizer

I feel no more or less germy than usual.

My entire trip to the dollar store cost $23.54, which felt good for the amount of stuff I purchased. Cutting everyday costs is often crucial to staying on budget and out of debt, so I’d encourage anyone who’s really pinching pennies to explore what their local dollar store has to offer. At the same time, it’s important to consider the selection differences among stores, compare prices ahead of time or know what quantity you usually buy things in. Despite the fact that I have a constant supply of Hershey’s Kisses in my apartment (seriously), I didn’t realize that a 9-oz. bag wasn’t what I normally buy, and I mistakenly thought I was getting a deal when I wasn’t. Smart shopping goes a long way in keeping your finances on track, so it’s worth it to pay attention to details.

More Money-Saving Reads:

Images: Christine DiGangi

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized