Being late on one bill can’t hurt your credit score that much, right? Wrong! Not only can a single, small late payment slice 100 points off your credit score, it can take three years to recover from the damage.

The roughly 60% of Americans who have excellent, 700-or-above credit scores, and who might think they don’t have to worry about those scores, should sit up and pay attention to this.

When the Consumer Financial Protection Bureau released its report on unpaid medical debts last month, a revealing sentence was tucked deep inside:

“An unpaid collections tradeline of at least $100 to a consumer’s credit report will reduce a score of 680 by over 40 points and a score of 780 by over 100 points,” it said.

Really? A single $100 late payment could drop a consumer from a 780 score to a 680 score? Could take someone from nearly perfect credit to a so-so score, potentially costing them thousands in borrowing costs?

I went looking for more information from both FICO and the CFPB about that sentence, and here’s what I’ve found: It’s true. So are a couple of other inferences you might draw from the CFPB report: The higher your score, the more a single mistake can cost you, and in fact, the longer it takes to rehabilitate your score back to where it was.

The CFPB got its information in an email from Fair Isaac, according to the agency. But that email just confirmed information made public earlier by FICO.

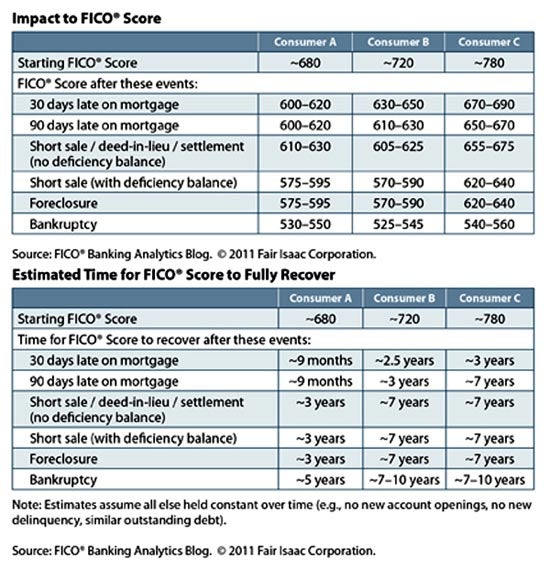

The Impact of a Late Payment

Fair Isaac calls the penalty after a negative event “damage points,” and in a moment, I’ll talk more about various damage points associated with negative credit events, along with the rehabilitation time required. But first, a more nuanced explanation of what’s going on.

FICO credit scores are the result of a complex formula that incorporates numerous credit-related events from your credit report. The number is dynamic, meaning it could be different today from tomorrow. The FICO folks will tell you that it’s impossible to say precisely what a certain positive or negative event might do to a credit score. Furthermore, keep in mind that there are dozens of different credit scores out there (from FICO and other companies), each with their own variation. So these numbers are merely guidelines, and not necessarily exactly what you would see if you pulled your own credit score.

“I would note that it is just meant to be a rough guide in terms of direction and magnitude of score impact,” Fair Isaac spokesman Jeffrey Scott told me. “Precise score impact is much more difficult to capture as it will vary depending on the credit profile of the consumer in question.”

That said, the rough guide is relatively precise, as described on this Fair Isaac blog post — which in this case explains the impact of late mortgage payments.

A consumer with a 780 score would drop to between 670 and 690 after being reported 30 days late on a mortgage, and wouldn’t return to 780 for three years, all other things being equal. A consumer with a 680 score, on the edge of prime, would be dropped to 600-620, landing in potential subprime status. The recovery time for that consumer could be only nine months, however.

Recovering From a Hit

What’s the lesson from this? Somewhere, we all know implicitly that we should be careful paying our bills if we plan to soon take on a major purchase, like a home or a car. You’d be smart to drop the word “soon” out of that equation. If you plan to borrow money within three years — and the way life works, it’s pretty hard to say that’s unlikely — you’d better not miss a payment. Ever.

If your blood pressure it climbing, here’s one important caveat: Being late on a bill is not the same thing as being reported as late to the credit bureaus. Not all creditors are quick to report late payments. Many will give you a chance to bring your account current before reporting you.

It’s best not to take that chance, however. Also, while it can take three years to recover fully from a late payment, the score does recover gradually during that time.

A few more notes from the chart: Being 90 days late on a mortgage is even worse than 30 days, but most of the damage is done by being reported late at all. Having an account sent to collections can result in additional damage points, though in the new FICO 9.0 formula, those collections damage points will be removed if an account is paid in full, according to Scott. Foreclosure or declaring bankruptcy is worse still, and the lingering impacts of that on a credit score can last up to 10 years.

On the other side of the ledger, you don’t have to be late to get hit with credit score damage points. Maxing out a credit card, which will impact your available “credit utilization,” can lower your credit score up to 45 points. That’s enough to impact your ability to get the best available rate on a loan. The good news with this issue is you can recover from credit utilization damage points simply by paying your bill, which restores available credit, and elicits a smiley face from FICO. To better understand how your credit score reflects your payment behaviors, it’s always helpful to regularly check your credit reports and credit scores to watch out for problems and track your progress. You can get your credit reports for free once a year from AnnualCreditReport.com, and you can get two credit scores for free, updated every 14 days, on Credit.com.

More on Credit Reports & Credit Scores:

- How Do I Dispute an Error on My Credit Report?

- What’s a Bad Credit Score?

- How Credit Impacts Your Day-to-Day Life

Image: iStock

You Might Also Like

Experian is a credit reporting agency. It also offers consumer cr... Read More

March 7, 2023

Credit Score

Do you keep a close eye on your personal finances? Or maybe you�... Read More

January 4, 2021

Credit Score

If you’re serious about your credit score, you need to pay your... Read More

September 29, 2020

Credit Score