Fighting with a credit reporting agency over inaccuracies isn’t easy, and plenty of consumers simply give up, a new Federal Trade Commission study suggests.

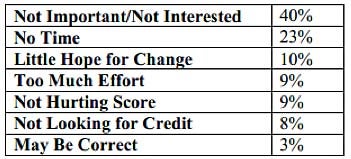

Nearly half of consumers engaged in an unresolved dispute with a credit reporting agency wave the white flag, according to a study published this week by the Federal Trade Commission. Of those who surrender while still believing inaccurate information persists on their reports, one-quarter give up because they “do not have enough time” to continue; 10% said they felt there was “little hope” for fixing the error. Another 40% say they gave up because they didn’t think the issue was important, or they had no interest in pursuing the matter.

“Most consumers who previously reported an unresolved error on one of their three major credit reports believe that at least one piece of disputed information on their report is still inaccurate,” the FTC said in announcing the results.

“(This) does not surprise me, it’s not easy for a consumer to file a dispute with the credit bureaus — the time, resource and energy commitment is significant,” said Chi Chi Wu, a consumer lawyer and credit bureau expert at the National Consumer Law Center. “An especially poignant example of this was in the first FTC pilot study, where a consumer with a material error in her credit report explained ‘she was a single mother with twins and could not muster the time to file a dispute.'”

The study, based on a sample of consumers’ credit reports the FTC has been examining for several years, aims to offer a glimpse at what consumers face when they believe they are being unfairly punished by an inaccuracy in their credit reports. The agency used experts to help about 1,000 consumers examine their credit reports and dispute any errors. Initial results, released in 2012, found that about 25% of the participants had errors on their credit reports, and roughly 5% of the participants had errors significant enough to impact their ability to obtain credit.

For this year’s study, the FTC re-interviewed 121 participants who filed unsuccessful disputes over alleged inaccurate information, calling those disputes “unresolved.” Of that group, about 30% of the consumers conceded they’d made an error, and they now accept the original information as correct. But the remaining 70% felt their disputes were still valid. About half that group said they are still fighting the error. The other half have given up, for reasons cited above, and in the chart below.

The report does have good news for consumers. A frustrating phenomenon known as “re-insertion” – which occurs when consumers successfully dispute errors, but they reappear later on their credit reports – seems to have largely been eliminated by the credit bureaus. The FTC found re-insertion on only 1% of reports.

On the other hand, consumers who don’t agree with the outcome of the dispute have reason to be frustrated: 41% say they were never notified that a bureau rejected their dispute, and of those who did receive notice, 48% said they were given no explanation for the rejection.

“We acknowledge the possibility that some portion of these ‘not notified’ consumers in actuality may not remember receiving the notice or may have thrown away the notice as ‘junk mail.’ However, this high proportion of consumers who claim no notification is noteworthy,” the FTC said.

Norm Magnuson, Vice President of Public Affairs for the Consumer Data Industry Association, said the dispute process that consumers can use today has been improved on since the 2012 study.

“We believe this 2013 eOscar© innovation, which wasn’t yet online in 2012 when the FTC study was conducted, ensures greater clarity in terms of disputes and reduces frustration for consumers and their lenders who want to serve them,” Magnuson said.

The FTC recommends consumers vigilantly monitor their credit reports for possible errors; a free annual credit report can be obtained at AnnualCreditReport.com. Consumers can also keep an eye on their credit reports by getting a free credit report summary for free on Credit.com, which is updated every 14 days, to look for problems that require a closer look at one’s credit.

More on Credit Reports & Credit Scores:

- How Do I Dispute an Error on My Credit Report?

- What’s a Bad Credit Score?

- How Credit Impacts Your Day-to-Day Life

Image: iStock

You Might Also Like

Find out if your rent and utility payments are reported on your c... Read More

April 11, 2023

Uncategorized

Becoming an authorized user is a common tip for individuals tryin... Read More

September 13, 2021

Uncategorized

Long-term unemployment can really hurt—and not just financially... Read More

August 4, 2021

Uncategorized