Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The amount of money you need for a down payment depends on the overall cost of the house as well as the type of loan you’re approved for. VA and USDA loans can be as low as 0% while conventional and FHA loans range between 3%and 10%. Jumbo loans typically require a 10%down payment or more.

Buying a home is a goal for many Americans. The consumer and market data experts at Statista expect over 6 million homes will sell in 2023, which is a great sign for the housing market. If you’re one of the millions of Americans planning on buying a home, the first question you may have is, “How much do I need to put down on a house?”

Today, you’ll learn about how much you’ll need to put down before buying a home, and it may not be as much as you think. We’ll also go over how your down payment affects your offer as well as the pros and cons of making a larger down payment to help you make the right decisions before purchasing your dream home.

What Is a Down Payment?

A down payment is a certain percentage of the purchase price that you pay up front to secure a property, and the rest is paid in installments as part of a loan. Buying a home is a major purchase that can be hundreds of thousands or even millions of dollars, and if you’re like most people, you don’t have that much cash lying around. A down payment is much more realistic amount to pay up front, and it also lessens the risk of the lender by showing you’re more likely to have the ability to make your mortgage payments on time.

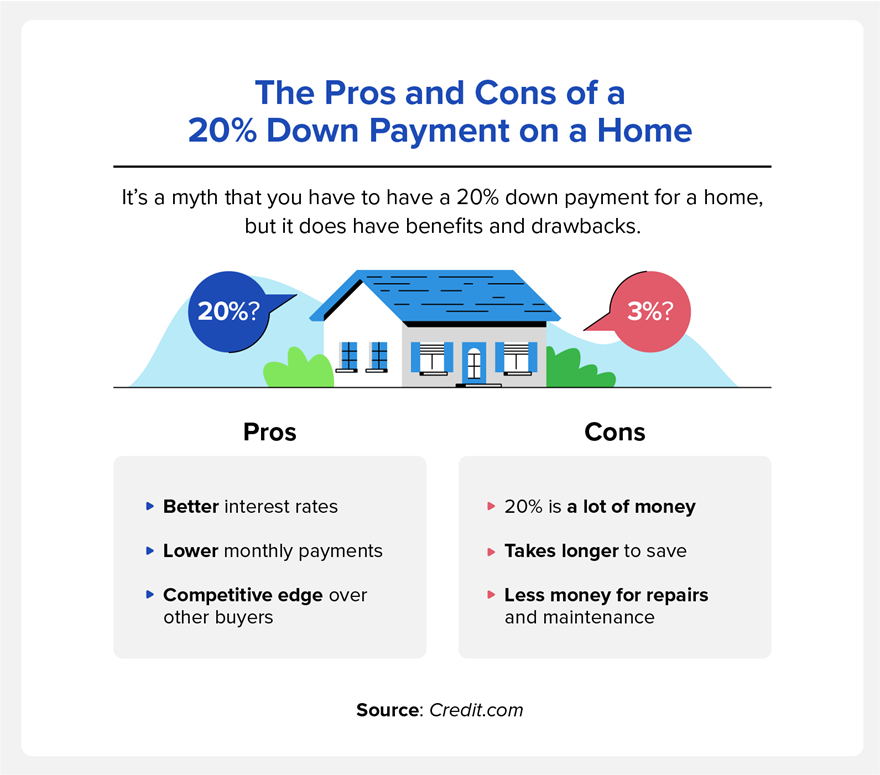

Do You Need to Put a 20% Down Payment on a House?

It’s a myth that you have to put down 20% when buying a home. A 2022 National Association of Realtors study found that 35% of people believe you need a 16-20% down payment to buy a home, but that’s not the case at all.

The data collected was from 1989 to 2021, and it shows that the typical down payment was 7% for first-time homebuyers and 3.5% for those getting an FHA loan.

The study also showed that repeat buyers put down an average of 17%, and this is because, based on their experience, they know the benefits of a larger down payment.

Although buyers don’t have to put down 20%, there are a few pros and cons to doing so:

Pros:

- Better interest rates: A larger down payment means less risk for the lender and a smaller loan amount, so they charge less interest.

- Lower monthly mortgage payments: The overall loan amount is lower, which also lowers the individual monthly payments.

- The offer may be more competitive than other potential buyers: A larger down payment makes sellers feel more confident in the sale because it shows you can access more money and make the payments.

Cons:

- It’s a lot of money you’ll no longer have access to: It’s always good to have a financial cushion in an emergency, so depleting your savings for a larger down payment may be a risk.

- It may take longer to save for a home: The difference between a 5% and 10% down payment on a house can be tens of thousands of dollars, which can take additional years of saving.

- You have less money for maintenance, repairs, furnishing, and appliances: Houses have many additional costs aside from the actual home.

- You will have to take out Private Mortgage Insurance (PMI) insurance.

Minimum Down Payment Requirements Based on Type of Loan

The minimum down payment for a house can vary depending on which type of loan you’re approved for.

- VA and USDA loans: If you’re a veteran or currently active in the military or qualify for a USDA loan, your down payment may be as low as 0%. The USDA loans are for suburban and rural home buyers and have an application process where you must meet certain requirements for the program.

- Conventional loans: These loans include loans like HomeReady and Home Possible and can be as low as 3%. These aren’t backed by the government, but they have similar guidelines and sometimes require a minimum credit score of 620.

- FHA loans: Federal Housing Administration loans are as low as 3.5%, but for those with bad credit, it may be 10%. To qualify for the lower down payment amount, you’ll need a credit score of 580 or higher.

- Jumbo loans: For these larger loans that exceed FHA limits, the down payment may be as low as 10%, but lenders often require more to lessen their risk.

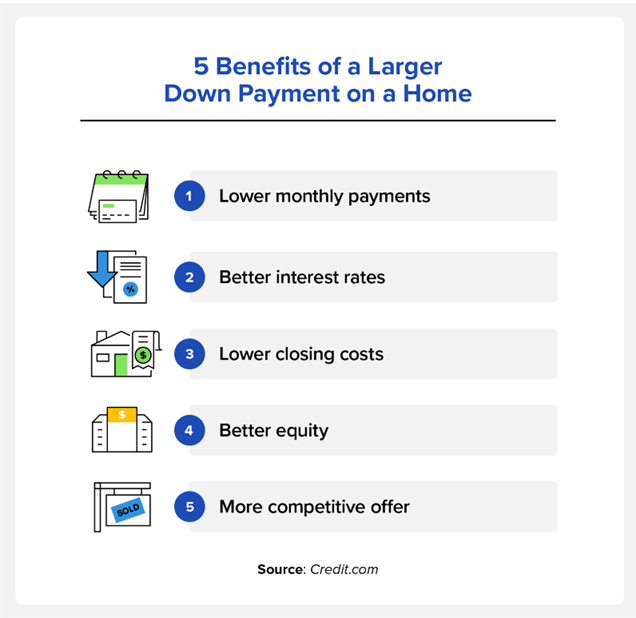

Five Benefits of Making a Larger Down Payment

If you know how much house you can afford and are in a good financial situation, a larger down payment is typically a better option. While 20% may not be achievable, there are still benefits to making a down payment that’s higher than the minimum.

The following are some of the benefits to a larger down payment:

- Lower monthly payments: Your monthly payments are divided by what you owe on a home, so a larger down payment will reduce how much you spend each month.

- Better interest rates: Interest rates are often higher when a lender is taking on more risk, so they’re lower when the lender is lending less money due to the larger down payment.

- Lower closing costs: Lenders charge closing costs as a percentage of the total loan amount, which is less based on the big down payment.

- Better equity: Your home’s equity comes from how much of the home you own, and you own more of a percentage of the home with a larger down payment.

- Better chance of closing the deal: Sellers feel more confident selling to someone who can put down more cash up front.

How Much Should You Put Down on a House?

How much you put down on a home is going to be different for everybody. Not only will it depend on your personal situation and financial goals, but it will also depend on how competitive you want to be with your offer. When buying a home, there may be multiple offers, and a larger down payment can signal to sellers that you’re able to follow through with closing the deal.

A larger down payment also means less money for other financial goals. In that same study from the National Association of Realtors, they found the second most common source of down payments comes from loans. If you’re already in debt when looking to buy a house, you may want to put down a lower down payment.

Here are some other considerations that may help you decide how much to put down on a house:

- How much you should keep in savings: Life is unpredictable, which is why it’s always good to have an emergency savings fund. When deciding on a down payment, it’s helpful to ensure you still have some savings to fall back on in case of emergencies.

- Other costs as a homeowner: Some first-time home buyers forget that they’ll have more expenses when owning a home than renting. You’ll be responsible for all of the maintenance and repairs.

- Closing costs: The closing costs of a home are a percentage of the loan, so when planning out the down payment, keep this fee in mind.

- Down payment assistance options: There are various programs and incentives for home buyers, so you may be able to find down payment assistance options. Also, remember that different lenders may have different rates, so shopping around may help you find a better deal.

FAQ

There are additional nuances to down payments on a home, so we’ve answered some common questions below.

Is It Worth Putting 20% Down on a House?

If you’re in a good financial position and can afford a 20% down payment, there are many benefits to putting that amount down. It can help lower your interest rates and monthly payments and may even help you close the deal with the seller.

Is $10,000 Enough to Put Down on a House?

A $10,000 down payment might be enough for a home. According to the National Association of Realtors, down payments are based on a percentage of a home with an average down payment of 7-17%.

What Is the Normal Amount to Put Down on a House?

The normal down payment amount for a house varies depending on the house’s price and loan type.

How Much Do You Need to Put Down on a 400K House?

The most common type of loan is a conventional loan, and you may put 5% down for a 30-year fixed-rate mortgage. For a $400,000 home, the down payment would be $20,000.

Can You Buy a House Without a Down Payment?

Yes. There are government-backed loans like VA loans or USDA loans that don’t require a down payment if you qualify.

How Your Credit Affects Your Ability to Buy a House

In addition to the down payment for a home, your credit score plays a big role in the overall cost of a home as well as the type of loan you can qualify for. For example, the FHA has credit requirements, and you need a score of 580 to qualify for a 3.5% down payment.

If you’re unsure where you stand with your credit, you can sign up and get your free credit report card right at Credit.com. We also provide additional services through our ExtraCredit® program that can help you monitor your credit score in addition to other features as you get ready to buy a home.

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages