Mortgages aren’t one-size-fits-all products. Loan types and lenders all have different requirements, benefits and drawbacks.

Some require sterling credit and sizable down payments. Others have looser standards but limit where you can purchase, or come with higher fees. Heck, one loan program is open to only about 1% of the population – the veterans and military members who proudly serve our country.

The type of mortgage can affect everything from your purchasing power to your monthly payment. The key is finding the mortgage program that makes the most sense given your particular financial situation, your homebuying goals and how you fit into the qualifying scheme.

To be sure, context and caveats are important when thinking about home financing. But sometimes just taking a cold, hard look at the numbers can also help provide clarity.

Running the Numbers

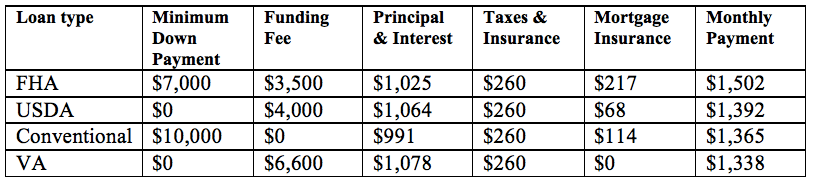

Let’s look at the four main mortgage options: conventional loans and the trio of government-backed mortgages (FHA, USDA and VA). Credit score requirements will be highest for conventional loans, typically followed by FHA and then VA and USDA.

Conventional borrowers will typically need to make a down payment of at least 5%, while FHA borrowers have a 3.5% minimum. Borrowers who can’t muster at least 20% down on either loan type will also pay mortgage insurance each month. Neither VA nor USDA loans require a down payment.

But all three government-backed loans have an upfront mortgage insurance premium or a funding fee. Most borrowers choose to roll these costs into the loan, which increases the monthly payment.

For our example, let’s assume you’re looking for a $200,000 mortgage at a 4.75% interest rate. We’ll use a consistent estimate for monthly property taxes and insurance.

At a glance, VA borrowers have the lowest monthly payment given the parameters. Conventional and USDA borrowers have similar payments, with FHA loans far and away the most expensive.

Parsing the Products

There are pros and cons to each loan type, however.

VA loans: Having no down payment is a significant advantage, although it also means you’re starting with no equity in the property. The funding fee varies based on service history and usage of the program. We used the highest possible fee (3.3%) for this example. First-time VA homebuyers would pay 2.15% and save even more money each month (and borrowers with a service-connected disability don’t pay it at all). As with the other government-backed options, the fee in this example is financed into the loan.

Conventional loans: These require the highest down payment, but you establish equity at the outset. The rate for private mortgage insurance can vary based on credit score, down payment and other factors (for this example, it’s 0.72%). There’s no funding fee on conventional loans, and borrowers can seek to cancel their mortgage insurance once their loan-to-value ratio is around 80%.

USDA loans: These feature no down payment and lower mortgage insurance costs, but the latter is payable for the life of the loan. These loans are also the most restrictive. Consumers must buy in a “qualified rural area” and have an income at or below 115% of the area median income.

FHA loans: This is often the loan of last resort. FHA loans have the highest monthly mortgage insurance costs, which borrowers will also pay for the duration of their mortgage. Credit requirements are looser, but borrowers who can work to improve their score and muster an additional 1.5% in down payment savings will benefit from pursuing conventional financing.

Weigh Your Options

Deciding which loan is right for you is a conversation that should include a good loan officer. Have them run the hard numbers and give you a clear breakdown of the benefits and disadvantages.

For example, VA loans aren’t automatically the best fit for every eligible veteran. Qualified VA borrowers with excellent credit and enough cash for a 20% down payment might get better rates and terms going conventional.

But that rosy profile is more exception than rule for VA-eligible borrowers, which is what makes this program so powerful for service members, veterans and military families.

Here’s the bottom line: Get a clear understanding of your options and the opportunities they present before pushing forward on a home purchase.

[Editor’s note: Checking your credit before you start looking for a home can help you determine whether you’re ready to buy. Giving yourself plenty of time to build your credit and get a higher credit score can help you qualify for better loan terms, and can save you money over time. Check your credit scores, which you can do using a free tool through Credit.com, to see where you stand. Then check your credit reports for errors that you’ll need to dispute, or problem areas that you need to work on in order to get your credit on track.]

More on Mortgages and Homebuying:

- Why You Should Check Your Credit Before Buying a Home

- How to Find & Choose a Mortgage Lender

- How to Get a Loan Fully Approved

Image: Gajus

You Might Also Like

Learn more about credit union mortgage options. Use this credit u... Read More

December 13, 2023

Mortgages