Q: How much does gallbladder surgery cost?

A: Anywhere from $5,865 to $94,897.

Here’s another one: How can a person with good insurance wind up paying $6,104.64 for gallbladder surgery? Well, it’s not hard.

We set out on this quest after hearing from Justin Evans, of Bonney Lake, Wash., who has pretty good employer-sponsored insurance, and who after his gallbladder surgery got bills for around $50,000. He is being asked to pay $6,104.64 as his responsibility, though he was in-network and his insurance has a $2,000 deductible.

Evans’ email said:

“On Jan. 11th, I underwent an emergency Gall Bladder removal surgery. It went extremely well and from the time I walked into the ER until the time I walked out after surgery was a total of 13 hours. I’m just now starting to get bills and it is ridiculous! The Hospital stay alone was over $44,000, for 13 hours! Insurance and adjustments left me with over $3,600 out of pocket for the hospital. That’s not to mention the ultrasound charges, xray charges, surgeon charges & anesthesiologist and any other bills I’ve yet to see. So far it’s nearly $50k in charges. I can’t understand how 13 hours in the hospital can cost more than my monthly mortgage for 4 years or the same price as a fully loaded BMW X5! … I’m just not sure why such a routine surgery performed between 500,000 – 700,000 times a year can cost so much.”

Evans, 35, is an operations manager for a machine and fabrication shop. His Premera Blue Cross insurance is through work, and all of his doctors, hospitals and others were in-network – as far as he knew, until he received a bill from an out-of-network emergency room doc service.

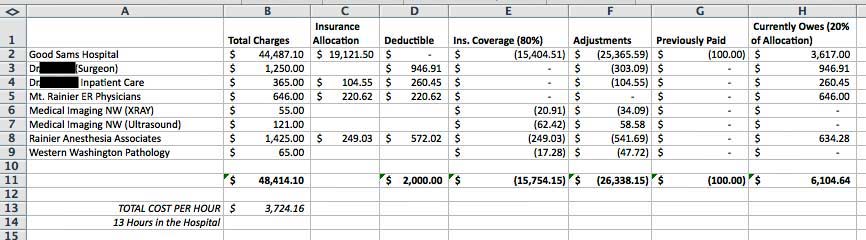

Evans made a spreadsheet of the prices and reimbursement rates, shown below.

Click to enlarge

First, Some Comparisons

At clearhealthcosts.com, we’re about to roll out a big dataset with cash or self-pay prices for bigger-ticket items, so we’ve learned a lot about what cash patients pay for things like gallbladder surgery.

At the Surgery Center of Oklahoma, in Oklahoma City, the price is $5,865, all-inclusive. So Evans could have gotten his entire operation for less than his co-pay, and also a round-trip airline ticket from Seattle to Oklahoma City, which is around $300, would have brought him in around $6,165 – just a smidge more than what he is being asked to pay – on top of the insurance company’s stated outlay of $15,754.15.

The self-pay price for a gallbladder removal at Rochester General in Rochester, N.Y., is $6,260.91, without anesthesia and doctor’s bill.

At the Banner Baywood Medical Center in Mesa, Ariz., the price for a laparoscopic gallbladder removal is $94,897 as a list price, but the self-pay discounted price is from $11,611 to $14,223.

One friend who lives in the New York metro area told us about her gallbladder surgery that had a total bill of $13,975.21 — and the insurance company paid $7,752.57 and she paid $1,111.52.

Finally, just below is a screenshot from his insurance company’s website explaining how much they estimated such a procedure would cost. They estimated $17,936 for his surgery at Good Samaritan Hospital in Puyallup, Wash., and he was billed $44,487.10. (I asked the hospital what their self-pay rate was, and they told me that their self-pay rate is the same as the chargemaster rate. However, they said they also offer uninsured patients “prompt pay discounts up to 40% by paying their entire bill within 30 days of the first statement.”)

Click to enlarge

What Cost Him So Much?

The hospital charged $44,487.10 – don’t forget the 10 cents! – of which his insurance company, Premera, paid $15,404.51. Evans paid $100 for this, and he’s being asked for another $3,617. That’s his 20%.

For the in-network surgeon, the $1,250 price means that Evans is billed for $946.91. (His deductible is $2,000.) And, he gets to pay another $260.45 for the surgeon’s in-patient treatment, although the doctor is in-network. Part of the in-network anesthesiologist also fell on his deductible, for $572.02.

Mount Rainier ER Physicians asks for $646, none of it covered by insurance. (They are not in his network, though the hospital is). He said he didn’t know they were out-of-network. We hear this a lot: in-network hospital, emergency situation, out-of-network docs or anesthesiologists (as if you are expected to ask, while lying on a gurney writhing in pain, “I know this is an in-network hospital, but I just want to make sure: do you take my insurance?”).

The X-ray, ultrasound and pathology bills are entirely covered by insurance.

A Closer Look at the Charges

With the in-network charges, Evans’s plan has an in-network individual deductible of $2,000, and an individual in-network out-of-pocket maximum of $6,000. His insurance leaves him responsible for 20% of the emergency-room costs, and 20% of an in-network emergency-room facility (with a $100 copay), inpatient facility and many other items.

So of the hospital bill, for example, he wrote: “Insurance covered $15,404.51, which is 80% of their allotted amount for service, which is $19,121.50. My ER co-pay of $100 brought that down to $19,021.50. My bill for the $3,617 is roughly my 20% portion of the co-insurance, there was about a $200 discrepancy, but it was overpayment on their end. The $25,365.59 that was waived was the balance that insurance wouldn’t cover and was basically known over charging.”

Evans emailed that he had received a call from Bethany Sexton, vice president of revenue cycle for Multicare, the parent of Good Samaritan Hospital, referring to his chats with me.

Evans raised with her his objections to what he regarded as a high bill. “We discussed the consequences of [my] not paying the balance and ultimately at the end of the 4th billing cycle (120 days) it would be turned over to collections of which it could affect my credit should the delinquency continue beyond 60 days with the collection company. We also discussed payment options and financial aid options [for] which she is sending me information.”

Evans considered having his bill reviewed by a professional for discrepancies, and disputing the bill, however he decided against it because his insurance company told him that even if some charges were thrown out, the insurer would still most likely allow that $19,121.50 and his 20% would remain unchanged. When he complained that it seemed like an overcharge, she told him that if the hospital reduced charges, and instead charged what it really cost, they would be leaving money on the table. There’s no incentive to reduce the charges, essentially.

Now when it comes to the out-of-network charges: Out-of-network providers can bill the insurance company whatever they want. Then after (or if) they get paid, they bill the patient for the balance (it’s called balance billing). You can appeal that with your provider and your insurer, and Evans has. In some states, laws protect consumers either by prohibiting this practice, requiring prominent display of signs showing that out-of-network providers are working at in-network facilities, and so on.

The Kaiser Family Foundation compiled the state laws about that. In Washington, in-network balance billing is not permitted, but out-of-network is.

What Can You Do Under the Circumstances?

First, you’re not alone. A recent Kaiser Family Foundation report found that one in three Americans had trouble with medical debt. Many of those are insured, but have issues like Evans’s.

“Just because you have good insurance that doesn’t mean you won’t have large out-of-pocket costs. Take the time to understand your insurance coverage and confirm that you are working with in-network providers if that will save you money,” says Gerri Detweiler, director of consumer education at Credit.com. “And unless it’s an emergency, shop around! Even with insurance, the cost you may wind up paying can vary tremendously.”

Here are some tips for dealing with medical bills.

- Keep all your bills. If you don’t get an itemized bill, ask for it. The bill from the provider and the bill from the insurance company should be compared for anomalies and errors.

- Know your insurance plan. Evans was surprised to see that his plan requires him to pay 20% of emergency charges. The plan language can be very confusing. If it’s not clear, ask.

- If you think that the bill or the insurance company payout might be wrong, go on record immediately in writing as contesting the bill and the payout. Procedures for this vary but a certified letter will establish a paper trail.

- Keep good records of who you spoke with and wrote to and when. Keep the names, phone numbers and other identifying factors: “Ms. Smith, Premera customer service, 216-xxx-xxxx, extension 1435.”

- Analyze the bill. Some experts say 20% of hospital bills have some identifiable error; others say the number is much higher, approaching 100%. There are services that will do this for you; they are generally called medical bill advocates. If you’re going this route, make sure you know what you’re paying for. Your HR department may be a good resource here.

So you have to pay?

“If the provider will allow you to make payments, that may be your cheapest option as most won’t charge interest,” Detweiler says. “Review the itemized bill carefully and question any charges you aren’t sure are legitimate. And don’t be afraid to try to negotiate. If you can come up with a lump sum — even if that means charging it — you may be able to knock a substantial portion off the bill.”

Detweiler adds that even if you are making payments, your bill could get sent to collections. “So always make those payments on time and reach out to the provider if you will be late. Monitor your credit reports and scores to make sure medical bills haven’t been sent to collections without your knowledge.”

The Consumer Financial Protection Bureau, a federal agency, has some tools. Your state insurance department, or your state attorney general, or the Better Business Bureau, may also be avenues of appeal.

Here’s another option that worked for one person: Our friends over at WBUR public radio in Boston wrote about a patient who appealed for a year a charge of $1,126 for a 2-inch bandage, to no avail. The patient posted the link for the story on the hospital’s Facebook page. The following day, the patient received an email from the hospital apologizing and granting her a $1,124 credit.

[Editor’s Note: If you’re worried about how medical bills could be affecting your credit, you can monitor your credit scores for free on Credit.com. Also, you can pull free copies of your credit reports once a year.]

More on Managing Debt:

- The Credit.com Debt Management Learning Center

- Understanding Your Debt Collection Rights

- Top 10 Debt Collection Rights

Image: nito100

You Might Also Like

Learn more about what a judgment is, how it works, and what the d... Read More

May 30, 2023

Managing Debt

Medical bills can be daunting. Around 67% of bankruptcies in the ... Read More

September 7, 2021

Managing Debt

Debt can feel like a terrible thing, but paying off your debts is... Read More

December 23, 2020

Managing Debt