With three young energetic boys, the growing costs of college education weigh heavily on my mind. As a financial adviser with a reputation to maintain, ignoring these pending expenses is not an option for our family. Each year, I share updated age-based benchmarks we use to ensure that our 529 college savings plan is on track to meet our goals.

For a child born today, expect the four-year costs of tuition, room and board, and books to run $196,496, based on average in-state tuition rates and a 5% annual increase. Reaching this goal requires a monthly savings of $448 from the day a prospective college student is born. Private institutions charge approximately twice this amount.

Parents have many different philosophies when it comes to preparing for college expenses. Many of those who are capable financially do not hesitate to foot the entire bill, but I think these parents are making a mistake. I see great value in having my children share in the cost of their education.

I am not going to let them take on a crushing amount of college debt. But I’m also not going to let this chance to think long and hard about opportunity cost pass us by. No matter how much you plan to contribute, letting your children in on the financial realities of college is one of the more important lessons they can learn from their college experience.

How We Determined a Savings Plan

My wife and I have decided to use in-state college expenses to target our savings. In Virginia, we are blessed with a long list of high-quality colleges and universities that have been subsidized by our tax dollars, and I want our children to think twice before looking elsewhere.

We’re planning to save 75% of these projected costs by the time they graduate from high school. I don’t expect we’ll ask our children to cover the entire remaining 25%, but we might.

They can pay their share with scholarships, summer jobs or subsidized loans (if Sallie Mae hasn’t gone belly-up by that point). Through some combination of natural talent and a strong work ethic, I don’t expect they’ll have any problem making this investment.

If it turns out that a college considers our boys as gifted as I do, we may not even need all the money we’ve saved. You may not know that you can finance your own retirement with any money not used up in college savings plans. The penalties imposed by taking money out of a college 529 savings plan are a wash when you factor in the tax-deferred growth of these plans. In fact, any scholarships your children receive will allow you to take money out of these plans without any penalty at all.

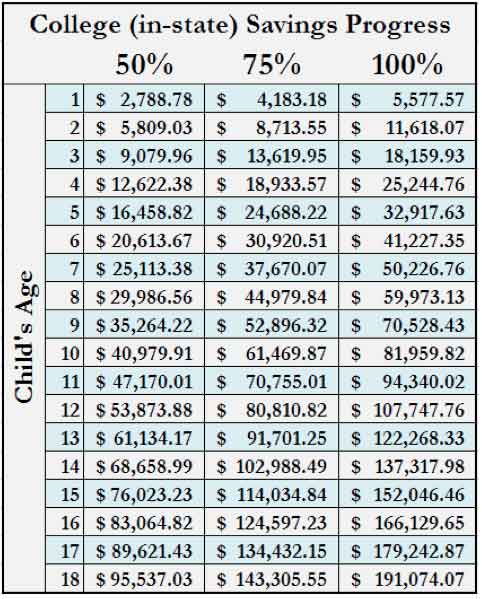

Tracking Your Goals

Use this progress chart to see if you’re on track to meet your college savings goals:

Parents following our 75% plan should have saved $24,688 by age 5 and $61,470 by age 10. The 75% college savings plan suggests a monthly savings rate of $336 per child from the day they are born. As I mentioned earlier, you can estimate private school costs by doubling these numbers.

The value of my college experience becomes clearer each year, and I have a strong commitment to help offer this opportunity to my children. I expect that advanced learning and networking will become even more critical in their future. If you have young children and haven’t started saving for their future college costs, make it a priority to begin a 529 savings plan today. Preparing for our children’s college expenses, or at least 75% of them, is a sacrifice well worth making.

More Money-Saving Reads:

- What’s a Good Credit Score?

- How to Get Your Free Annual Credit Report

- What’s a Bad Credit Score?

- How Credit Impacts Your Day-to-Day Life

Image: david franklin

You Might Also Like

There are many ways to put money back in your pocket throughout t... Read More

April 17, 2023

Budgeting and Saving Money

Studies show the majority of adults in America can’t c... Read More

April 3, 2023

Budgeting and Saving Money

Find out how much the average family has in savings compared to w... Read More

March 8, 2023

Budgeting and Saving Money