Credit’s a tricky thing. Some things obviously hurt your credit, like a late payment or no payment or maxing out your credit cards. But the effect of some things on your credit isn’t obvious at all and are almost counterintuitive. Those things seem like they should help your credit but can actually hurt. One of those things is closing accounts. But are closed account on your credit report bad? Well, yes. But why?

Closed Account Are Bad for Your Credit

Yes Virginia, closing an account, such as a credit card account, can hurt your credit. But why?

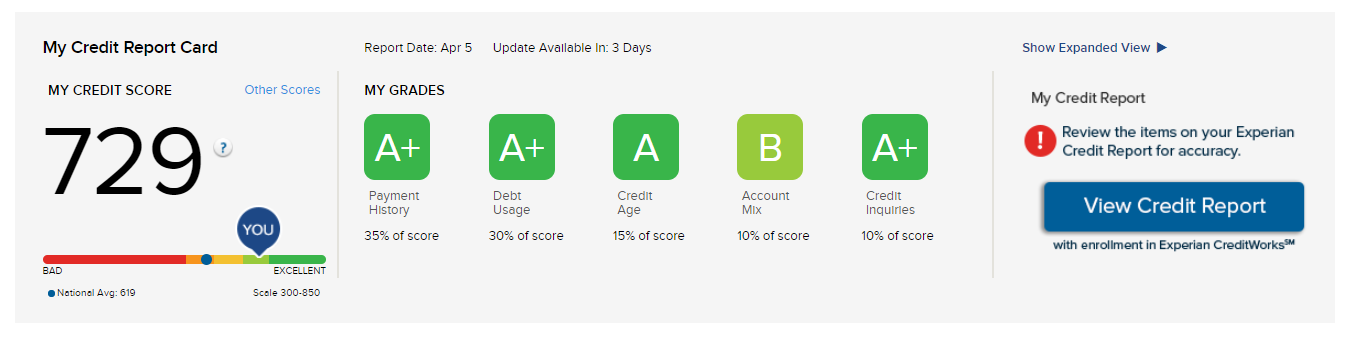

There are five key areas that are tracked on your credit file by the major credit bureaus:

- Payment history

- Debt usage or credit utilization ratio

- Credit age

- Account mix

- Credit inquiries

The credit bureaus run credit scoring models against those five factors to calculate your credit score. Payment history makes up roughly 35% of your score, debt usage 30%, credit age 15% and account mix and credit inquiries 10% each.

And while it may seem like closing credit cards is a good idea. It’s actually as hurtful to your credit as missing payments. Closing an account is a triple threat to your credit score as it impacts your:

- Credit utilization rate—AKA debt usage

- Credit age—AKA credit history

- Account mix

That potentially 55% of your score that’s impacted by closing an account—20% more than missing a payment that affects your payment history. Ouch!

How Closed Accounts Hurt Your Credit

Just how does closing an account affect so many areas used to calculate your credit scores? Here’s how.

Closing an Account Hurts Your Credit Utilization Ratio

“Revolving utilization” is the amount of your revolving credit card limits you’re currently using. So your available credit limits compared to your actual credit card balances. For example, if you have an open credit card with a $2,000 credit limit and a $1,000 balance then you are 50% “utilized” on that account because you’re using half of your credit limit.

The same applies if you had one credit card with a $1,500 limit and one with a $500 limit and balance of $1,000 across both cards. In other words, your total credit limit and your total balance(s) are what matters.

Credit card issuers, lenders and the credit scoring models like to see your credit utilization ratio at no more than 30% and ideally no more than 10%. Having a ratio of 30% or less is almost as important to your credit scores as making your payments on time. As the ratio increases, your credit score decreases.

The assumption is that the more you charge, the less responsible and therefore riskier you are.

But where does a closed account come in? Well, an open account adds to your credit limit. A closed account subtracts from it. And when you close an account, that account’s credit limit no longer applies toward your credit utilization ratio.

So, in the example above where you have one card with a $1,500 limit and one with a $500 limit, if you close the one with the $500 limit, but still have a $1,000 balance, your credit utilization ratio jumps from 50% to 67%! That’s 17% farther away from the 30% max that lenders and creditors want to see.

Bottom line, it’s better to keep the account open and not use it or only use it sparingly.

Closing an Account Hurts Your Credit Age or History

You’d think credit age was a simple measure of how long you’ve been using credit in general. Not so. It’s actually a measure of how long you’ve had any given account or loan. And while closed accounts don’t immediately fall off your credit report, they do fall off sooner than open accounts.

In most cases, negative credit information stays on your credit files for seven years from the date the debt first becomes delinquent. Positive credit information can stay indefinitely. Closed accounts in good standing are usually removed from the credit report within 10 years after closing. And while credit scores continue to benefit from the positive history associated with an account for as long as it remains on the credit report—open or closed—once the account is removed from your credit report all of that history is gone.

And the credit scoring models favor a long credit history. Consumers with a younger credit history are seen as riskier borrowers than consumers who’ve had credit for a longer time.

Bottom line, hang on to those old accounts by leaving them open. Keeping them open doesn’t mean you have to use them—although you want to make sure the issuer won’t close the account if you don’t use it. If they will, simply use that account one year or so for a small purchase.

Closing an Account Hurts Your Account Mix

Lenders and creditors like to see well-rounded consumers. They don’t want consumers with only credit cards and no loans. And they don’t want consumers with only loans and no credit cards. That mix of different types of accounts—revolving credit and installment loans—is your account mix.

While you can’t realistically extend the term of an installment loan. For example, extending a 30-year mortgage to a 45-year mortgage. You can keep credit card accounts open so you have a beefier account mix. And if you don’t have any installment loans, consider taking out a small personal loan just to add to your account mix now and again if needed and assuming it won’t cause you financial issues. Even an auto loan is an installment loan. If you can swing a 0% loan for your next car, that can be a beautiful boost to your credit score.

Note too that open accounts are included in your account mix. Open accounts are those that are paid off monthly, such as utilities, your cell phone, and charge cards.

When to Consider Closing an Account

Sometimes closed accounts on your credit report aren’t as bad as the consequences of keeping the account open. Cases, when it may be best to close the account, include:

- The account is a joint card with a former spouse, business partner or another person that you need to sever ties with and/or who creates a financial liability for you.

- You tend to overspend and the temptation of the account is too great.

- The account has high recurring fees, such as a credit card with a high annual fee.

Can You Reopen a Closed Account on a Credit Report?

You don’t have a lot of options to re-open accounts closed due to delinquency. You can though ask that an issuer re-open an account that was in good standing but that you chose to close. The credit card company may update the status of the original account to open or make create a new account. You can ask which approach it uses. Reopening an old account can build on your established credit history.

Where Is Your Credit?

To find out where your credit currently stands, you can check all three of your credit reports free once a year at AnnualCreditReport.com. If you’d like to know your score and keep an eye on your credit more regularly, Credit.com’s free Experian credit score and credit report card gives you an easy-to-understand breakdown of your credit report’s details using letter grades, along with free credit score updated every 14 days.

You Might Also Like

Experian is a credit reporting agency. It also offers consumer cr... Read More

March 7, 2023

Credit Score

Do you keep a close eye on your personal finances? Or maybe you�... Read More

January 4, 2021

Credit Score

If you’re serious about your credit score, you need to pay your... Read More

September 29, 2020

Credit Score